Part 3: What will be the wider impact of a bust in startup valuations? Scroll down for parts 1 and 2. A quick reminder. Private investment dominates the current boom in startup funding. Public traded stocks play a much smaller role than in the past. For example in the dotcom bubble most big companies went to IPO. One point of view is that this will contain the impact. A lot of private investors will lose money. But the fallout for the general economy will be small. I don’t think this will happen. I will explain at the end why this will be a good thing. But warning this next bit is a real downer. “There are some things you learn best in calm, and some in storm” Playing for High StakesFor a start there is just too much money involved. Mattermark identified more than $100 Billion of US investment over 10 years. This only covers rounds over $100 million. Globally the numbers are huge. The private investment factor amplifies the pain of losing. There is no liquidity in private markets. Investors cannot bail out if they see the downturn coming. Or even after it has hit. No-one can cut their losses and run into safe havens. Mark Cuban made this point in a recent post. Startups are not a portfolioA bigger factor is the herd mentality. Most other assets classes offer shocking performance. Big institutional investors are counting on startup investments to beef up their total returns. Much of the money derives from the same sources that piled into sub prime and the like. The problem is that institutional investment tends to adopt a herd mentality. It doesn’t matter if they are right or wrong. Too many investment adopt the same strategy. This makes the whole system vulnerable to shocks. This factor is also amplified. In this case by a misunderstanding of portfolio risk. You will see a lot of advice about the risk of investing in early stage companies. Invest in a large number of opportunities and the big winners will offset the wipeouts. Build a portfolio they say. This is not a portfolio. This is a buying a lot of tickets for the lottery. It may well work and it has for many funds. But it is not spreading risk. Every investment just adds another high risk. Pick enough and one will pay off is the theory. The problem arises when the lottery stops paying out. There is no balance in the portfolio. Everything turns bad. Remember this is how it will be. Even the big quoted companies destined to join the corporate elite will experience large falls in value. Its not just about the moneyLets not forget that it is not all about finance. A downturn in startups will also have wide impacts because this stuff matters. People and businesses rely on the software startups produce. The network feeds itself and consumers love it when it does. Enterprises are creating massive value by using mobile and digital to do business better. Mobile money, mobile health and green startups are changing the world. If some of these companies fail, people will care. Big knock on effects are possible. Many apps interconnect through APIs. Your business does not just depend on the software you have. Other applications and data sources are integrated. Sometimes these are invisible to the user. Consumers are in the same position. A Matrix of Possible OutcomesSo what will the impact look like? This is harder to understand. We understand how a big bust in public markets transmits to the wider economy. Because this is a bit different, the mechanism is less well understood. In reality we don’t know. What follows is educated speculation. I have not attempted a systemic analysis just picked out some specific possibilities.

Green ShootsBut the tech industry will emerge stronger and better from everything that happens. A startup valuation bust will be a beautiful thing for entrepreneurs as I wrote in part 1. It will also be great for the whole ecosystem. A downturn is a real opportunity for innovation. The best ideas emerge from the furnace of hard times.

New HorizonsThere will also be big opportunities for individual entrepreneurs and investors. Remember two basic principles:

The startup ecosystem will shrink a bit. Those who are left will be the people with real vision and passion. A few years after the bust the industry that emerges will be bigger stronger and better than ever before. Writing these articles has reminded me I love startups. A real focus on change for the better and a great ecosystem of people to work with. These basics will not change if times get tough. I like to share the latest ideas for building a great business. If you would like these direct to your inbox, subscribe below. Thanks for bearing with me through this series.

Comments

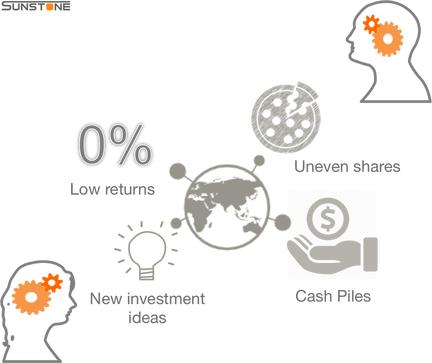

This is part two of a series of three articles on the impact of a bust in startup valuations. For part one read down below. For part three…be patient. Valuations and the real economyMattermark published a fascinating blog post in January. It explores the connection start up investment and US interest rates. Do historic low rates fuel explosive growth in funding? The article explores various trend correlations which support some basic economics. Extreme low yields (zero in the case of interest rates) will give a high nominal price. For any stream of earnings. Fred Wilson of Union Square Ventures explained the theory in depth in March 2014. 0% Interest drives high startup valuationsThis essential fact lies behind one of 3 megatrends. Together these have created the current funding landscape. Another way of looking at the first trend is to consider alternative forms of investment. Look at four major traditional options. Public equity markets, public debt markets, property and physical assets, and business investment. Returns on the first two categories are at historic lows. Debt markets are flooded by Government debt. Real interest rates have turned negative in many countries. Stock Market Indices are high but this reflects a lot of money chasing a small pool of return. P/E ratios are also in record high territory. The picture for property appears more mixed. This is because the focus tends to be on capital values. But the explanation for the rapid recovery of property values is the same. It is a reflection of diminishing returns. I admit that this trend is patchy with a heavy concentration in narrow markets. Think London and Silicon Valley. Cash is piling upBusiness investment is a window on two of our megatrends. In most developed economies, levels of business investment remain low. Business owners are refusing to invest because the returns are too low. Many corporations have huge piles of cash on their balance sheets. But they are not spending. The supply of cash is growing at an amazing rate. The US, UK and Japan have all printed epic amounts of money in the last 5 years. The US is now calling a halt (or at least a pause) but the EU is just about to start.  This cash is not distributed in a broad or deep spectrum. The mechanism of QE is not a direct one. As a result, most of the printed money is sitting in 3 places. Corporate balance sheets. Sovereign wealth funds from commodity producing countries. And non banking financial institutions. Policy and regulation are keeping banks starved of funds. At the same time both private and public investment vehicles are awash. Little or nothing is trickling down to the bottom of the pyramid. Thomas Piketty’s treatise on inequality is a thorough reflection of this trend. New investment opportunities emergeA huge increase in cash concentrated in few hands. Historic low returns on many forms of investment. These trends create the conditions for massive investment in new structures and forms. This is exactly what we see. Our third megatrend is the current startup funding world itself. It is different from previous booms. Money is being invested through private vehicles. Much of the cash is institutional, corporate or from wealthy individuals. But it is hidden from the public markets. This means there is no liquidity. Investors cannot retrieve their cash. As Mark Cuban points out in this post, a fall in valuations of investments with no liquidity will be very painful. Where will the signal come from...This was going to be two articles about the impact of a correction in startup valuations. "Why the startup funding bust will be a beautiful thing” looked at the impact of a bust on startups. Part three will look at the wider economic and social changes a bust might bring. When I started writing I discovered that I needed this bit as well. Context is important. Changes in the direction of these trends will be the signal for the correction. When this signal is sent and how long it takes to transmit are big unknowns. In one view it could take a long time. In Europe the situation looks just like Japan 30 years ago. That has not unravelled yet. This applies to all Europe not just the Eurozone. The UK happens to be ahead but... We live in a dangerous worldOn a different view a dramatic turn could happen fast. The current fall in the oil price might be that early signal. Severe disruption caused by political factors is also a live possibility. Public statements from politicians and the media are depressing. In proper democracies are led by people who appear to understand nothing. Public discourse about the challenges on the borders of Russia or in the Middle East is verging on puerile. To describe most media coverage as First Grade level would be an exaggerated compliment. Other possible flashpoints - West Africa, the Horn of Africa, Korea/Japan, SE Asia. Not even on the radar. Startups could cause their own downfallWe must also acknowledge that startup ecosystem could be the cause of its own bust. People have come to rely on software in both personal and business lives. Many apps are interconnected in a web of APIs and integrations. A severe failure in the wrong place could cause massive disruption. Loss of trust and faith would cause investors to hold back. Valuations would fall.

Failure is not the only possible problem. There is a whole industry of naysayers just waiting to jump on a privacy breach. Security and integrity are vital to all our futures. Even a small problem could be magnified in the wrong circumstances. Again the issue is loss of trust and faith. Investment depends on sentiment as well as spreadsheets. Watch with interest. Tech start ups live in a global economy. It is one of the benefits of the digital revolution. That brings responsibility. Everyone in the ecosystem needs to pay attention to global trends. I am not an economist or an “expert”. My view could be way off. But there will be a down turn. I would love to hear what innovators and entrepreneurs think could be the cause.  Map of the South Sea Bubble c1720 One thing is certainThis week has seen a several interesting posts about money. Authors highlight the unusual funding structure of the current startup boom. The basic point is that most of the money invested is private. Many entrepreneurs and early investors prefer to avoid the public capital markets altogether. This Quora answer from Keith Rabois explains why the IPO is out of fashion. The result is large funding rounds for mature companies with established revenues. But the risks of this type of investment are much greater than listing on the stock exchange. Bill Gurley set this out in his article. It also means that investors money is tied up for long periods. Institutional Investor claims that VC funds now have a life expectancy of 14 years. The normal planned exit is after 10. Huge flows of money have resulted in fast rising valuations for start ups. There is plenty of speculation that we are seeing a repeat of the Internet 1.0 bubble. One thing is certain. There will be a correction. That is the logic of markets. Whatever the "fundamentals" prices will fall at some point. This raises two interesting questions: 1. Who will lose out and what might be the wider economic impacts? 2. What changes will startup entrepreneurs and teams experience? I will try to answer the first question in a future column. This one is about question 2. The money switch tripsThe fund raising environment will change. This is pretty obvious and it will be the first thing most people notice. Meetings with investors will become rare. VCs will announce they are “changing their investment strategy.” AngelList’s homepage will display far more pitches with much less progress. Talk about lack of deal flow will stop. This switch will flick overnight. When it happens do not deceive yourself. The money will not come back for a long time. Trailing round chasing the vanishing puddle of cash will be a mug’s game. The ecosystem evolvesOf course the startup ecosystem is not just about money. There is a lot of other support around. Incubators and accelerators, Universities, public bodies, mentors and advisors. All are investing time, expertise and sometimes a bit of cash. A downturn in valuations will show you who is making a strategic choice. And who is just jumping on the bandwagon. Advisors will be the first to disappear. Professional services is an industry that has to chase short term cash. Not everyone will walk away but many will. Mentors will split. Those who have committed will double their efforts. Others who are just exercising their egos will stop taking calls. I just hope that Universities and public bodies will stay in the game. If Government investment is worth anything it must be for the long term. The number of incubators and accelerators will shrink. The survivors will only focus on real business quality. Hubs built around creating great pitches and raising funds will not make the cut. Culture shiftsStartup culture will experience a more subtle change. Today it takes a lot of determination and resilience to be a successful entrepreneur. The challenge will multiply in a downturn. Lots of startups are nurturing. Many try to live real values and ethics. The investor spotlight will turn on the perceived costs of these attitudes. The great businesses will not be tempted to change. Strong and sustainable culture is essential to long term success. One big risk as the culture shifts. Diversity is already low but could be a major casualty. Women, minorities and those from less blue chip schools or family backgrounds could easily lose out. To everyone, don’t let this happen. Please. Cash is King...The work and social environment will change fast. You will feel it immediately and most of those feelings will be negative. But none of these changes matters that much to a startup. The big one is cash crunch. The harsh reality of commerce will reassert itself. No money, no business. ...long live the KingReduce burn, get cash positive or die. At the same time keep margins rising and aim for higher growth. This will be the day to day operating environment. The pressure will increase as investors feel the pain. Angels and VCs will demand cash distributions. Dividends, interest, loan repayments. Only the very strongest will survive. They will share three things:

And beauty came like the setting sun:There is no way of writing this that does not sound negative and scary. There will be a lot of casualties and not all will deserve to fall by the wayside. But the outcome will be beautiful.

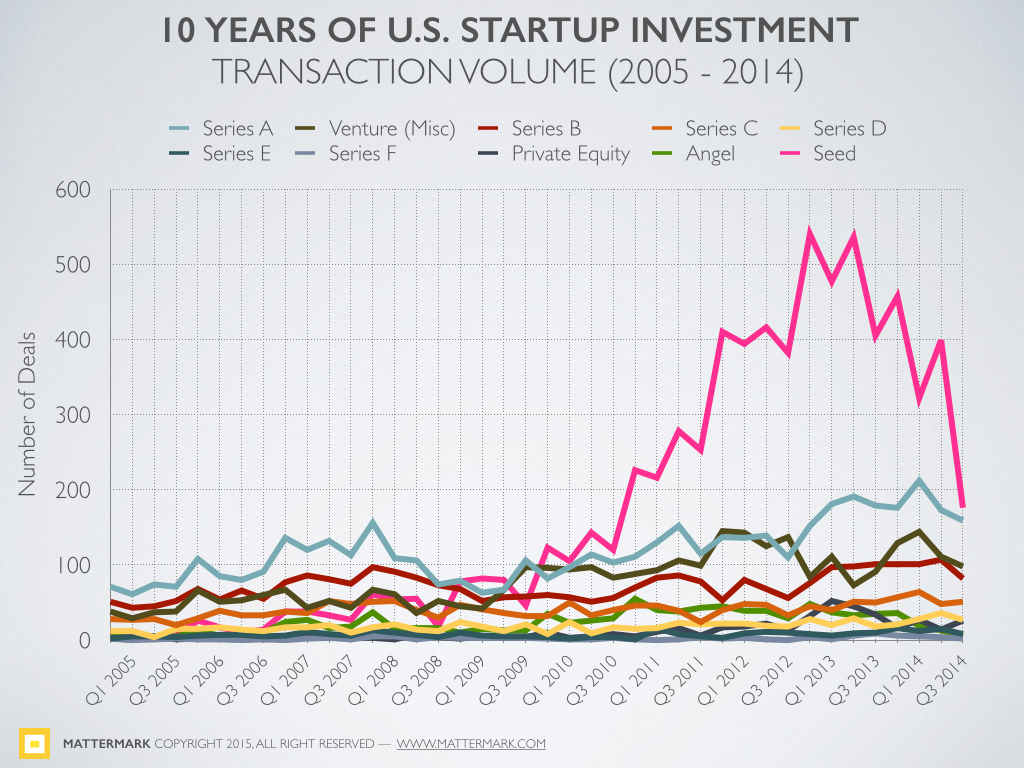

When the sun rises the landscape will be clear and simple. The tech industry will have created the next generation of greats. They will not be unicorns. They will be the companies that made it into the ark. That worked as teams and maintained their values. The ones that will change the world. How can you build a great business that will have the strength to survive? What advice would you give to an entrepreneur when the easy money dries up?  On the surface the investment outlook for technology start ups has never been better. VCs invested $48.3Bn (Money Tree Report) in US start ups last year, a whopping 60% increase year on year. Most of this torrent of cash went into software and biotech companies. Start up investment has become one of the hottest business trends across the world with Governments and commercial bodies vying to establish incubators, accelerators and other schemes. Seed funding is actually fallingA couple of recent reports have highlighted a trend underlying this growth which gives cause for concern. Mattermark (@mattermark) published an analysis of all funding rounds in the US over the past 10 years which shows the number of seed rounds falling from a peak in Q1 of 2013 back to 2010 levels. CrunchBase (@crunchbase) has taken this further and looked at data from the next 7 largest countries by number of Internet users. Both the number and value of seed rounds have dropped significantly in 2014. Investment is shifting from seed rounds to large Series A or later financing. What is happening?I don’t believe there is any shortage of innovative ideas and new entrepreneurs entering the market. If anything I expect that statistics on new business starts will show tremendous growth once again in 2014. Many of these start ups will share the ambition and commitment of their recent predecessors. This is one of the roots of the trend towards larger, later financing. Building a world leading company takes time and money so investors are in a longer cycle. Investing larger amounts for longer cycles also puts a strain on investment capacity. Start ups have attracted funds in recent years because other investment classes have offered very poor returns. As traditional investment options start to recover in at least some large countries, especially the US and UK, this inflow of new funds may slow. Anecdotally, I know of a number of Angel syndicates and VCs who are mainly preoccupied by follow on rounds. Follow on investment may also be going to quite well established businesses with a proven and profitable business model. Such companies just need working capital to fuel growth. This role has traditionally been filled by bank lending but at least in the UK there is little sign of this tap being turned back on. As a result, more funding from private sources is occupied with companies at this stage of maturity. It would be very interesting to see data on the level of exits. Larger investments with longer payback cycles will ultimately lead to a shortage of liquidity which will put further strain on the front end of the investment chain. Why is this a problem?The risk is that a funding gap emerges. Founders will continue to bootstrap and incubators will provide enough resources to allow all sorts of people to get companies started. VCs and other private investors will continue to show interest in companies that have a viable product and some traction. Bridging the gap between early stage accelerators and product launch/ validation could become a real problem.

Tech EU is currently running an excellent series on companies that have grown large without any recourse to external funding. You can see the latest instalment about Cleverbridge here. Are we entering a phase where managing without investment will become a key business skill? I would love to know. Are you seeing the same trends in start up investment that these reports highlight?  "I don't get it"I listen to start up pitches as an investor, a mentor, an advisor or a judge several times a week. Whenever there is an audience of two or more people, at least one person will struggle to understand how the business presented will make money. The answers are not usually clear in the business plan. Naturally the next step is to ask the entrepreneur. The explanations rarely satisfy the audience. The mobile and digital world does not have the basic concepts and tools to describe a successful business. The communication gapRemember this is typically an audience of smart, experienced business people. Most founders are passionate, articulate and talented. This is not a problem of quality, preparation or process. There is a real gap in communication. Pitches are all about communication. Founders create excitement by offering innovation and catch the attention of investors by showing growth. But entrepreneurs struggle to paint a picture of how their start up business will work. Obviously this is a problem for investors who are trying to assess the potential of a new business idea. It is also a problem for start up founders and entrepreneurs. Without a clear model for how your business works, how will you make the best strategy and management decisions? Analysts find it even tougher. There is no common set of metrics to evaluate and compare businesses in the digital world. How business models can helpThe business model is the solution to these problems. A business model is simply a set of activities and interactions which define how the engine of a business is constructed (statics) and how it drives performance (dynamics). Business models emerge from the practices and structures which work commercially. Successful and lasting models provide commercial opportunities all along the value chain including clear wins for customers. Good business models also work well within society to deliver wider benefits. We already know what worksMobile and digital technologies have led to an explosion of innovation in software. We have now reached the stage of maturity where 6 clear business models have become established. Some are well tried in technology (licences, eCommerce) others are borrowed from very different environments (SaaS, usage, advertising) or rooted in in our oldest commercial traditions (marketplaces). We have enough knowledge to describe how these 6 models operate. With a little effort we can measure the activity of each model and show how that activity links to financial performance. This gives you a toolkit to assess the organisation, management, control and prospects of your business using one of these models. It is then only a short step to paint a clear picture for an investor. The picture will help investors and analysts arrive at a structured evaluation of your business and provide a basis for comparison with your peers. What's in your toolkit?Understanding the underlying business model and managing performance using this knowledge is not a substitute for innovation or a constraint on new ideas. Think of business models as a toolkit or a set of APIs that let you unlock management and performance experience and use that knowledge to build a better business.

Which business model could help you explain your business? How could you use that model to run your business better?  In the startup cauldron cash flow and burn rate can feel like the only financial measures that matter. You must keep focus on the kitty to survive but money in the bank is not how your business generates value. Many founders find it hard to pin down the measures that show progress in value creation. There are a number of ways to look at this but one common approach is to understand and measure customer lifetime value or CLV. The fundamentals of CLVSimply CLV is the total revenue you will receive from a customer over the whole time that individual or company is your customer (R) less the direct cost of sales to that customer (C) less the cost of acquiring that customer (A). R-C-A=CLV. It should be obvious that this matters to any business but it is especially important to many startups. For pretty much any business model, R-C needs to be greater than A. If not then the cost of acquiring a customer exceeds the benefit and you cannot hope to generate value. Note in this case that a customer and a user are not the same. Google for example has millions of users who contribute no revenue. This is fine so long as there is also a market of paying customers. CLV can be a measure of value creationOnce you understand how much value each customer generates then you can start developing a long term model of business value and capital requirements. If 10,000 customers generate £10 million of CLV for example you can estimate the running costs and for a given amount of sales and marketing investment you can figure out how long it would take for your business to reach this number of customers. While this rule of thumb works for many businesses, it is especially useful for SaaS or other subscription based models. CLV provides a window on operational metricsCLV can also be a guide to understand which operational measures really matter. Every startup today has a bewildering variety of analytics at their fingertips. Which need to be monitored constantly and which are just interesting? In a fairly typical freemium SaaS business for example, A will be calculated by looking at the cost of sales and marketing divided by the number of customers that sign up and then multiplied by the rate of conversion into paying customers. Once the business has enough information to estimate the rate of churn, this can be used to estimate customer life. So if you lose 20% of your customers every year, typical life is 5 years. Multiply this by your average monthly revenue and hey presto you have a value for R. Now your SaaS business can focus on number of sign ups, cost per sign up, conversion rate, average subscription and churn rate. Track direct costs every month and you have the complete model in 6 figures. Of course each of the numbers in this kind of model is tough to estimate. When you start out you don't know how much your customers will pay or for how long. Figuring out how much it costs to sign up 100 customers might be quick but how many of those turn into loyal customers paying regular money? The risk increases if you need to employ a sales force to acquire customers. Use seed funding to test CLV potentialThese are all great questions. In my mind the purpose of raising seed funding is to answer them as robustly as possible. Test out how much it costs to acquire customers. Get feedback on what people will pay and how you can improve the design to make them more loyal - from a CLV point of view a year of extra usage may be worth more than a 10% increase in price for example. Demonstrate you can scale your product and your team to meet demand and that you know how much this costs. Build a CLV model to demonstrate valueOnce you have a robust proven model you have a basis on which you and other investors can make projections about future growth. You can show how you would spend that £5 million Series A round and calculate the value your business would create as a result. Your company will still be a high risk investment but you will have a model to work with at least.

Different companies require different approaches but CLV is a widely understood and applied concept. Build a model that demonstrates how your early progress creates CLV and you will have a great conversation with potential investors.  Well intentioned illusionsThe Startup world is home to many well intentioned illusions. One of these is the concept of "investor ready." This apparently attractive phrase is dangerous because it misleads about investor priorities, it misunderstands the relationship between investors and companies and it misrepresents the role of advisors. Let me explain. If you search the Internet you will find literally thousands of blogs and articles by angels, VCs and investors of all types setting out their investment priorities. Investor ready is never on the list. There is a very simple reason. Investors want to invest in a great business. The common factors - team, product/ market fit, growth potential etc - are all about being a great business. Investors and Startups need each otherInvestor ready also implies, even assumes in some cases, that Startups are supplicants aiming for the grace and favour of investors. This is wrong. Investing in a Startup is a partnership. The investor has scarce resources of money and expertise but the Startup also offers something rare, great people and an innovative business. Investors need Startups as much as Startups need investors. A few things you need to knowA mini industry has grown up around matching these needs. If you are a Startup looking for money, you will encounter this sector of the economy sooner or later. Here are a few things you need to know:

Hold onto your dreamThe most essential thing is not to lose yourself and your business in the “investor ready” process. I have seen many pitches and business plans (which is just another pitch remember) refined and improved by expert advisors which are designed to answer every question in the book. Unfortunately this never works. Once investors see the pitch sooner or later they will ask the question about the business fundamentals that is not in the book and the founder will be exposed. Your job in the investor ready process is just another pitch. It is not to change the market, the product or the revenue model to meet someone else’s expectation.

Securing investment is an exciting moment for any business. Remember you are an equal partner in that investment and what you bring is the idea and the passion. Lose these and the investment will be and for you and the investor. Keep them and we will all have fun. Summertime is famously quiet in the deals market - sell in May and go away as the old saying runs. While this is true in that few deals close and very little money changes hands, the sunshine and showers still bring out many conversations about fundraising in the Startup world. I have met with at least five interesting founders who are preparing to pitch for capital in the autumn over the past few weeks. Each approach is different and the amounts, purposes and frankly quality of the prospective investments varies widely. They have one thing in common, all have reached a narrow conclusion about the source of funding to pursue. Some have considered other options in detail, some barely at all. At some point it is necessary to target a clear pool of potential investment but these chats have made me think that it might also be worth restating the breadth of options that are available to start with. BootstrappingThe first source for most people is bootstrapping. This is a funky word for using your own money or cash you can raise from immediate friends and family. On the plus side, you will retain complete control of your business and all the returns will flow to you. You will also be taking on all the risk and unless you are very fortunate, the total amount of capital available will be limited. Nonetheless, it is always worth asking whether you can bootstrap to the next stage. People are giving it awayMany of the entrepreneurs I know have supplemented their initial funds by entering the wide range of Startup funding competitions and/ or applying for grants and accelerator or incubator support. We are well served in all three categories here in Scotland and the largest competition fund for Startups, the Scottish Edge Awards, has just received a boost from Sir Tom Hunter who is putting up £700,000 alongside the fund of £2.5 million committed by RBS. Between them these types of funding are a great way to progress from a business idea through to something that is at least viable. Becoming involved with accelerators or incubators can also be a great way of building your network and even extending your founding team. Choirs of angelsIf and when a Startup needs external funding the first port of call in many cases is business angels. In many cases this is just a small group of people, usually experienced business people, who have some reasonably serious cash to spare. One of the great benefits of this type of funding is that it often brings much needed experience, contacts and expertise as well as the hard cash. In the UK the angels can also benefit from substantial tax benefits in the form of EIS and Seed EIS. Not every founder has a book of contacts containing the names of a bunch of people flush with cash. Fortunately many angels have also joined together in syndicates. The formality of these groups varies considerably from a very clubbable feel to something very close to a VC fund. In all cases they provide a single point of contact who can access funds from a group of investors. You will still need to convince enough of those investors with your pitch but it can be easier than finding your own group of investors. However, many syndicates also charge fees and the level of support and advice provided varies considerably so this solution is not for everyone. In Scotland, business angels and especially angel syndicates can also provide access to an even deeper pool of funds through the Scottish Investment Bank an arm of Scottish Enterprise. SIB acts as an investor in its own right but in most cases it uses a process called matching to provide an amount of funds equal to that raised by angels. Most of the main angel syndicates are approved matching partners so the process can be very simple. Smart money or following the crowd?Of course in all of these investment cases, the investor will expect a share in the company. Deals vary widely but something between 10 and 25% is normal. This means your investors are also partners in the success of your business which in turn means that you will need to work with them for the long term. In many cases, this is a great relationship but it pays to be choosy about who invests. Resist the temptation to take the first offer of cash because finding the right people to work with is just as important as raising the money. Some businesses avoid the relationship element altogether by pursuing the crowd funding approach. With the arrival of equity crowd funding options this is now practical for many more Startups. In practice, most of the successful sites are pretty busy so it can be hard to stand out. Typically the crowd does not bring the types of networks and experience that angels or syndicates bring so it is not smart money. Despite these drawbacks, it is a real option for many founders. Where a consumer product is involved it may also be a great source of initial customers and a way of testing out pricing and feature options. The costs and fees involved tend to be pretty similar to most angel syndicates. In fact some of the best known crowd funding options are effectively angel syndicates put together on a deal by deal basis. Keep the whole pieNot everyone wants to sell part of the equity in their business. Two other options remain. One is loan funding. This can be very tough in the present climate with banks unwilling to lend even to established businesses. There are some publicly sponsored schemes, for example the West of Scotland Loan Fund, which offer attractive rates and may be easier to access. The Scottish Edge Fund is also introducing a loan element. Alternatively, your business could generate enough cash to fund itself to growth. This is not easy and will not be possible in every case. There is almost an unspoken assumption nowadays that a successful early stage business will not make any money. I have seen many business plans where this is indeed true and the founders need to build a huge market first before worrying about profit. There are exceptions though and it is worth thinking through whether your business might fit in this category. You can choose the road to takeAll of these options may only take you so far. Once a business reaches a certain value then serious money comes into play - Venture Capital, Private Equity, Listings and major Trade Sales. Often these options are exits for both founders and angel investors but not always. If you want to be the CEO of a global giant then you will stick with it through one or more of these stages as well. Whatever you do with your business, it is worth considering all your options at every stage.

A Cambrian moment for Startups - The Economist How Should Startups Approach Corporations?Canon has just announced the $150 million acquisition of Milestone Systems, a Danish software company specialising in video surveillance. In the same week, HP used its annual Discover event to trumpet Helion, a portfolio of Cloud products and services aimed at taking on Amazon’s market leading cloud offerings. Another story which caught the eye was an analysis of IBM’s network of support for Startups in Africa which now encompasses Smartcamps in four cities. All of these stories have a common denominator. The tech industry faces immense disruption and established players are trying desperately to find ways to adapt.

Startups have a vital role to play in this process. Of course, they are the prime source of disruption but they are also at the centre of change within the tech industry. Acquisitions, acqui-hires, partnerships and incubators are all strategies adopted in response to the threat of the mobile and digital revolution. This means the big, slow moving giants of the industry are not just easy targets for Startup founders. They are also a source of funding, market access and a potentially lucrative exit route for investors and founders. How can Startups take advantage of these opportunities? Begin at the end. Acquisition by an established player - a trade sale in the jargon - is by far the most likely way to a lucrative exit for Startup investors. Once you have a clear idea of your value proposition, it will often be quite straightforward to identify a small number of companies which are likely buyers even though the exit may be five years or more away. These need not be restricted to the tech industry. Mobile and digital technologies are disrupting business models across the board. Although in many industries, the market leaders are less aware of the threat and much slower to adapt. Nonetheless, retail, advertising, health, financial services and many others may be a good source of possible buyers. Look into the areas of investment and development that companies are pursuing. Often this will be publicly announced. Even if not, a quick glance at the type of investments made in recent years should give plenty of clues. I spoke to a couple of senior executives from large corporates recently and security, networks, cloud, analytics and big data all came up as areas of focus. If there is a clear exit strategy, the next question is how to start building a relationship with the target acquirer. Incubators or similar schemes to help Startups are a great place to look. I know of at least three Startups that have been through an initial bootcamp funded by Microsoft in Scotland or Germany and all continue to receive help and attention from the company. Even if the incubator option is not available, keep an eye on the partner programmes that large corporations run. These can be a great route to market and therefore a great growth accelerator. They are also one of the prime sources of acquisition. Many corporates rely on recommendations from product teams to identify partners that would make suitable acquisition targets. Even if none of these routes is available, just enquiring and meeting with executives from potential future buyers will help build valuable relationships. The Startup ecosystem is diverse and being noticed is a key part of success. How can Startups best take advantage of the disruption they are causing? I would love to hear your thoughts in the comment section below. Startup Investor Manifesto aims to set the agenda A group of Tech Entrepreneurs launched the Startup Investors Manifesto at the EBAN Conference in Dublin this week - you can find it here.... In the week of the Euro elections it is a pertinent reminder of the importance of entrepreneurship to all our futures.

The Manifesto is designed as a lobbying document and aimed solely and squarely at the various EU authorities. It follows on from the Startup Manifesto published a couple of years ago and like that document it is very much about startups in the tech sector. Initially it felt slightly odd reading it through. I am a startup investor and these people are lobbying on my behalf without me realising I was part of such a group. On the other hand, why shouldn’t the views of a vital and dynamic sector of the economy be strongly represented to Government and regulators? One answer to this question might be that Government interference in highly competitive markets is not the best solution. I totally sympathise with this sentiment but it is not actually how free market economics operates. If you want to see a totally unregulated free market, go to Mogadishu ( which by the way is not quite as scary as you would think…) Free markets depend on an open but reliable and predictable regulatory framework to exist and grow. For example, the stock market changed utterly when joint stock companies became an authorised vehicle for business in the middle of the 19th century. It is therefore very important that Governments create the right platform for startups to thrive and for investors in those companies to deploy their capital. An important proviso. The market framework should keep distortion to an absolute minimum. Does this manifesto propose measures which would help achieve that objective? Perhaps predictably it is a bit of a mixed bag. Some ideas are excellent, some are questionable and a couple of the proposals sound quite dangerous.

Overall, the main recommendations make sense but there are a couple of things in the detail that are major concerns. Firstly, the manifesto recommends a standard common definition of a business angel. Indeed in section 5.2 it actually says that this should be imposed. The whole point of angel investing is to encourage people with from every walk of life with the widest possible range of interests and agendas not to create a new defined (and no doubt regulated) class of investor. Secondly the detail goes quite a bit further than the broad agenda and starts to feel like quite a heavy hand and an element of protectionism ( the proposed transatlantic trade treaty is seen as a threat for example). Ultimately, if things go too far they risk strangling the very dynamism they are trying to encourage. Enough of the negative. Broadly I would support this initiative. I would like to build on it and in the spirit of the entrepreneurial movement to see recommendations which encourage broader horizons in three main ways:

I wish the promoters of the Startup Investors Manifesto well in their attempt and I hope they can find a way to include the ideas and the support of the whole community. |

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016