|

People are the heart of any business. In a startup there is often little else. A few lines of code and some sketched designs. Doesn’t amount to much. The ideas, the passion, the execution all rest in the people. This means people skills are not an option for a founder or CEO. Without the ability to build relationships, learn from other people and get the best from your team you will fail.

Any startup leader will be practicing these skills every day. It is part oft he dynamic in all their activity. In my experience most of them have a natural talent for this sort of thing. As well as being an integral part of the job, that talent is needed in two key situations. Growing people and hiring people.

This is not going to be a post about the hows of leading people. I wanted to set the scene. And then focus on one key point. The basis of success in any aspect of leading people…. Its about strengths not weaknesses

Most people have a kind of intuitive model for managing others. Every individual is good at some things - strengths. And not so good at others - weaknesses. Human nature then triggers a simple thought process. If we want someone to improve we need to fix those weaknesses. Seems obvious right?

Conscious or not this approach is endemic in all kinds of business. And it undersells your people and your organisation. We all succeed by honing and building the things we are good at. Becoming great at the stuff we know how to do. And excelling at what we love. In a surprising number of cases people become the best in the world at what they do Think about it. You didn’t leave school and focus on the subjects you were no good at. You forgot all that stuff and became the best you could. I always remember a friend of mine from high school. We were in the same class for English but nothing else. I was good at numbers so maths and science were my real strengths. I ignored the language stuff. (This should be obvious to anyone who reads this stuff regularly). But my friend found English was his best subject. He made a career as a journalist and became the editor of a national newspaper. He took his strength and made the best he could of it. Which turned out to be outstanding. Why change this thinking when we leave school? Great companies are built on this principle. Support great people to do what they do best. As a leader your first task is to identify the strengths of your people. When you are hiring you have little time with the candidates. Invest it in figuring out their strengths. Get to know what people can do. Not just technical skills. Are they potential leaders? Great team members? Social catalysts and influencers? Deep thinkers about the world? These are the qualities that will add value to your business. Making strengths count

You can do this every day. Great leaders do it every minute. You can also take a different approach to 4 other situations:

A focus on strengths means a different thought process for weak areas as well. We all have them and beyond a certain stage of life they are tough to eliminate. Instead of obsessing about perfection look for other solutions. Find a way to cover weaknesses by defining roles that allow others to fill in the gaps. Structure projects and teams to offer a good variety of talents. Try to keep things in balance rather than attempt the impossible. When you are hiring look for honesty and self awareness. Bring in people who understand their own strengths and weaknesses. You need to take account of those weaknesses. And place them in jobs that fit their talents. Why would you hire someone for a job they don’t suit anyway? But the purpose of the hiring process is not to catch people out. Try to understand the whole person. You will get great value out of people when you can see their talents and put those to work for your business. The strengths revolution

If you want to see the benefits of this thinking, check out the Genius, Power, Dreams programme run by my former colleague Andy Woodfield.

The difference may appear quite subtle. But the impact is profound. You need everyone to do awesome things and grow with your business. It is the hidden agenda for startup success. And I promise the most rewarding thing you will ever do as a leader.

Comments

I spend a lot of time with startups. Mainly in Scotland. Where we our unique history binds a country on the fringe of the world deep into global innovation. We are proud of our two unicorns. And there are some amazing founders and businesses. Its tough to generalise - I met Alba Orbital who make satellites this week for example. But the most common business model is a subscription SaaS company aimed at SMB customers. That’s why I write about this stuff so often.

And it niggles a bit that a lot of SaaS analysts focus on the challenges of the SMB market. Every other week I read an article somewhere that argues that you must target the enterprise to achieve SaaS growth. Most of these posts are written by people smarter than me. Yet I can’t get away from a sense that they are missing something. That the economics of SaaS for SMB work. In a niche for sure. But also at scale. I have one fundamental and rational reason for this. SMBs are a huge market. As this Edinburgh Group report shows they contribute 51% of the economy in the developed world and 67% of employment globally . This week I found time to do some digging into the real economics of the businesses that might serve that market opportunity. Here is my thinking on how the unit economics of SMB SaaS could support a great company. Maybe even a few more of those one horned white horses. What do the base numbers for SMB SaaS look like?

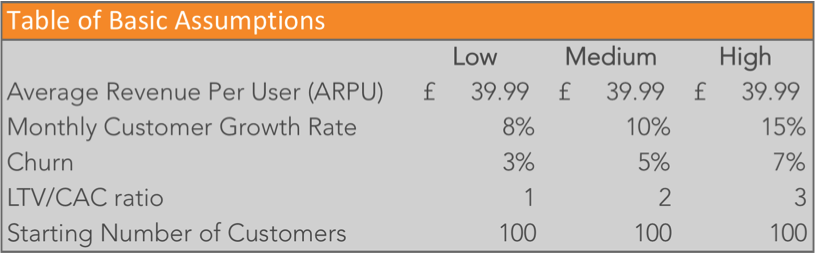

As a starting point we need to pick some numbers to model the unit economics. These are averages or benchmarks. Not because you should aim for them. Just to give a representative idea of how a “typical” SaaS business works. The base levels for the analysis below came from:

I have summarised these assumptions in the table below. Showing the high, medium and low (HML) points for each assumption.

What follows is a whole lot of messing around with these numbers. If you don’t have the time or the appetite to follow this take away just these messages:

Analysis 1: Growth rates

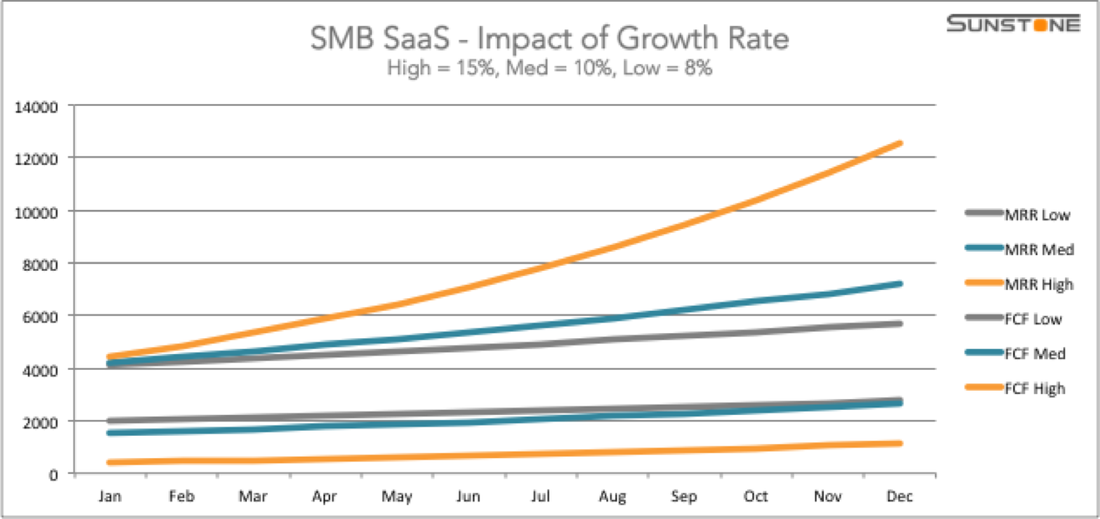

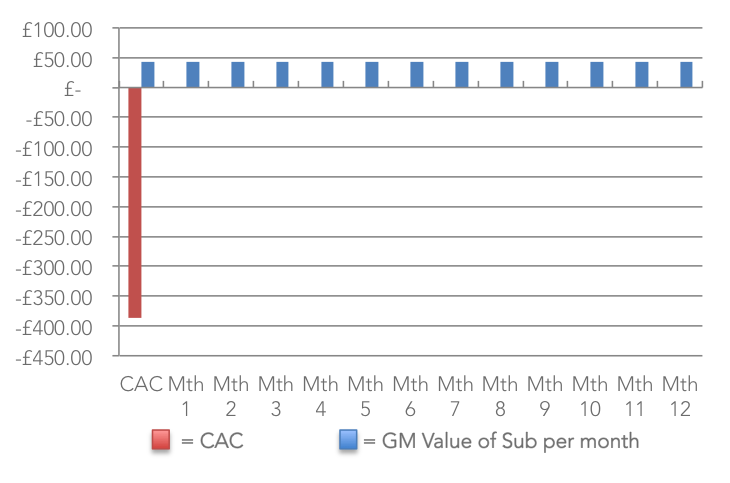

Now let’s start looking at the impact of different trends in some of these basics of unit economics. I will start with the simplest variable which is growth rates. The graph below shows the impact of H (15%), M(10%) and L(8%) growth on monthly recurring revenue (MRR) and free cash flow (FCF). I have used revenue not gross margin. For small SaaS companies storage and processing costs are in effect fixed cost. Not variable with revenue. As you grow you should switch to gross margin for this type of analysis.

FCF is defined as the difference between the cash paid by customers and the CAC spent each month to acquire new customers. In this simple example cash paid and MRR are identical. Because I have assumed all customers pay monthly. We will examine the impact of upfront annual subscriptions later. The other main assumptions are constant across all the HML variables. Churn is 5% in each case, LTV/ CAC ratio is 3. ARPU at £39.99 and opening customer base of 100 are the same for all graphs.

This tells us two things. No surprise that the higher your growth rate, the faster MRR increases. By the end of just one year you can see that the High growth option is pulling away from the others fast. If you play with the numbers you find that 15% is around the minimum for the start of a hockey stick to occur within a year.

FCF works the other way around. Faster growth needs more cash to keep the users flowing in. This would change if the LTV:CAC ratio was better for higher growth instead of fixed at 3. This is an important lesson. High growth can arise either from a more efficient sales model or spending more money. If you are struggling to match the cash raised by your competition, the only answer is to be smarter. And the LTV:CAC ratio is the key metric to track. Analysis 2: Churn

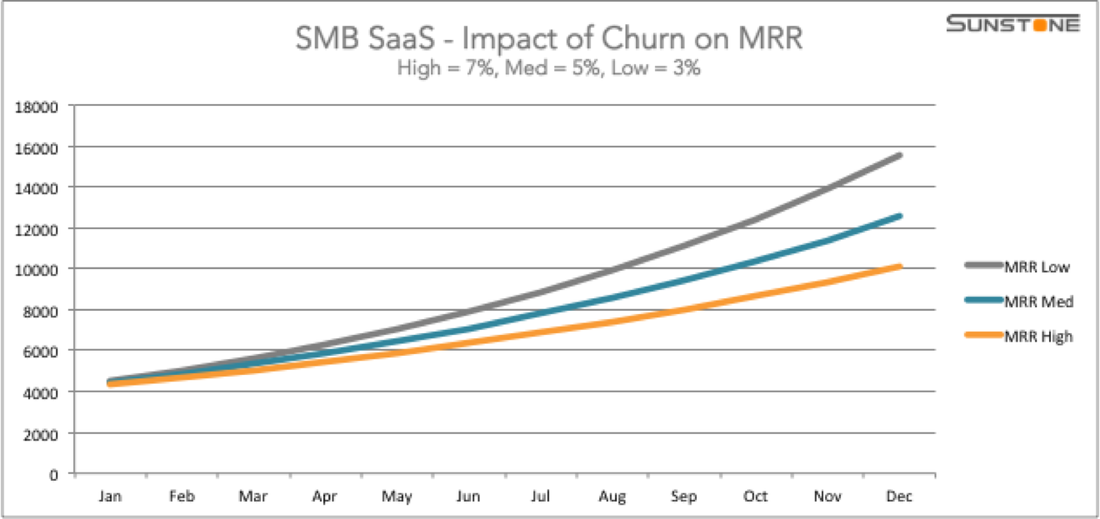

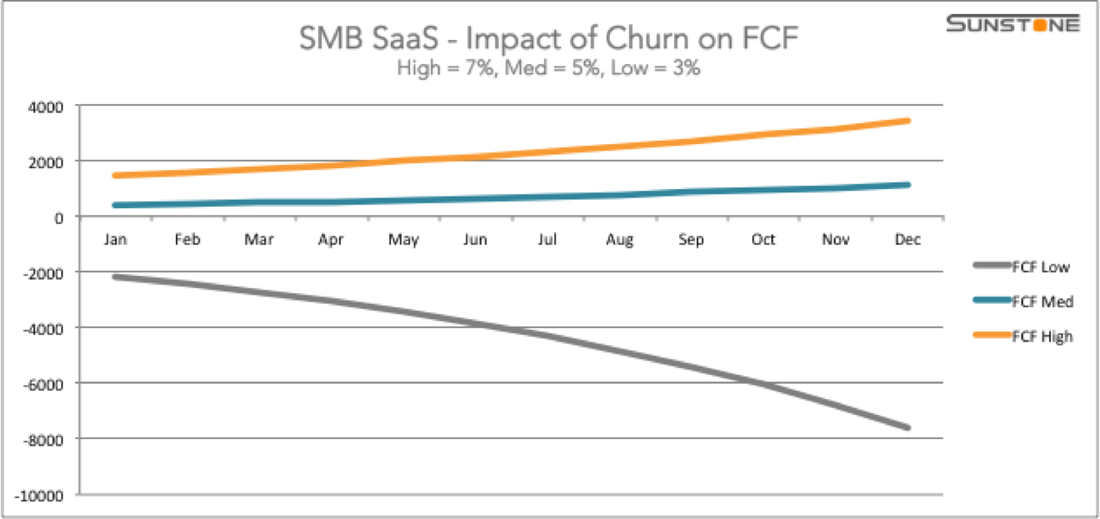

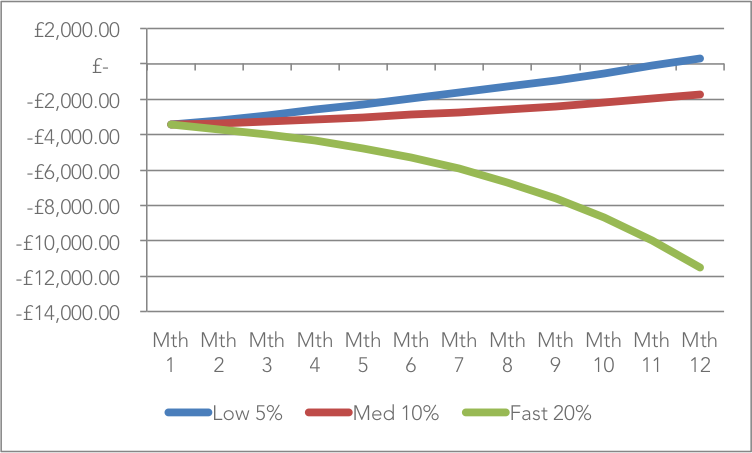

What about churn? Lots of analysts think this is a key factor in SaaS success. Lets fix the growth rate at 15% just so we get a little hockey stick at the end. The graph below shows MRR at H (7%), M (5%) and L (3%) churn.

Here we see a spread of outcome which pretty much follows the spread of churn. Losing customers matters pretty much in proportion to the rate of loss. Keep an eye on churn but don’t get it out of proportion.

One important caveat. I have used churn in customer numbers here. In a SaaS company where the range of ARPU is quite narrow this makes no difference. But if your highest paying customers represent a significant portion of your revenue then MRR churn matters more. The bigger your customers the higher the likelihood that this will be the case. This will also have a big impact on your sales model. Upsell to existing customers is much more important with an enterprise customer base. Before we leave churn let’s take a look at another effect. If we use the same HML for churn and the same 15% growth rate and fix the LTV:CAC ratio at 3, look what happens to FCF.

Wow! That looks totally wrong. Cash flow gets worse the better churn gets? This is where a small understanding of the dynamics of metrics and ratios could save you a lot of money. Churn is used to calculate LTV. The normal formula is just ARPU/ Churn % = LTV. As a result lower churn gives higher LTV. If we fix the LTV:CAC ratio then higher LTV is an automatic translation into higher CAC .

Simple lesson. LTV:CAC ratio matters but so does the absolute value of CAC. If I fixed the value of CAC instead of the ratio we would see the same pattern for FCF as for MRR. Reducing churn is a good thing. But don’t allow your CAC to drift up at the some time by focusing only on the ratio. Analysis 3: LTV:CAC Ratio

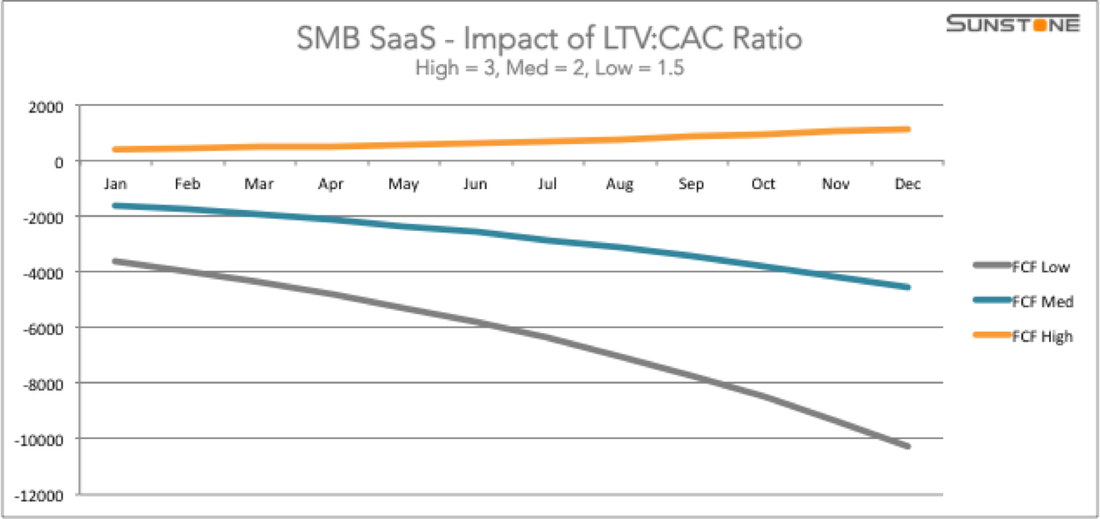

Let’s take a look at that ratio. The 3:1 target is rough and ready. Anyone I have read recommends it and then add that there is no rationale behind the number. What impact does it have if we start changing the ratio?

This only affects FCF. MRR does not vary with the LTV:CAC ratio. I have stuck with the 15% growth rate for all 3 scenarios because this is cash hungry. Churn is fixed at the median of 5%. I also see no point in modelling a ratio of 1:1. In this case by definition you are never making any money so something has to change.

It turns out that 3:1 is right on the button. Below this level (1.5:1 or 2:1) cash burns fast. At 3:1 you can stay FCF positive - just. For your SMB SaaS ever to get to cash positive, 3:1 is the minimum ratio. Get there and keep improving is critical to a sustainable business. Analysis 4: Beware the discount factor

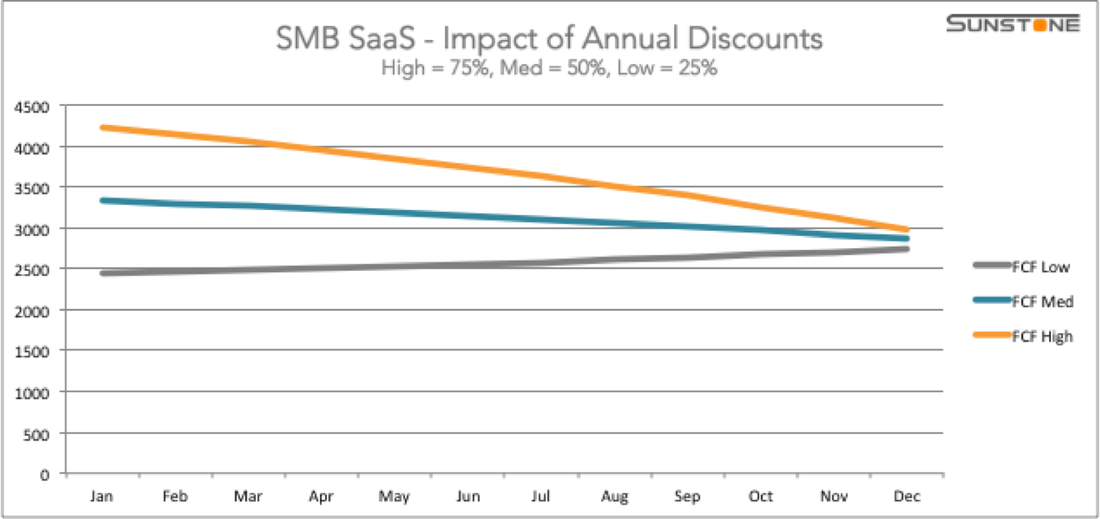

One final analysis of dynamics. Everything so far has been based on monthly subscribers paying every month. Most online SaaS offers packages to tempt payment in advance. Usual approach is a discount for paying a whole year upfront. The argument is that this boosts cash flow. How does this work out in practice?

Another sobering picture. I have fixed the other elements as usual but based on 10% growth. The pattern for 15% growth is the same but extends out over 2-3 years - this allows us to see the effect in 12 months.

The discount element is also fixed. I have assumed 10 months for the price of 12. Again a common approach. The most frequent in the sample of companies I looked at. HML here is about the percentage of new customers paying annual upfront - H (75%), M(50%) and L(25%). The higher percentage gives a big boost upfront. But it narrows fast. MRR shrinks the more you discount. If I laid MRR onto this it would show that MRR in the High scenario was 8% lower than in the Low option. Discounts are for the short term. They can produce a much needed cash boost. But keep your eyes open. The benefit is short and the bar for revenue gets higher with every giveaway. How big does SMB SaaS need to be?

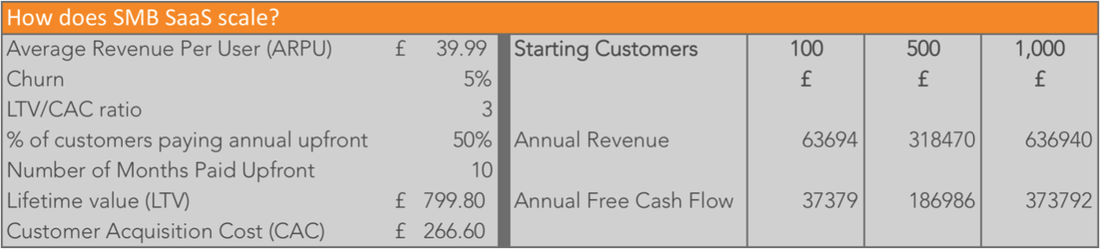

The conclusion so far is simple. The unit economics of SaaS for SMB work. You can generate revenue and cash flow provided your CAC is under control. Yet these numbers deal only with free cash flow. You need to build and maintain a product. Proceed customer service and support. Do all the boring admin stuff that you need to run a business. And make a living for the founders. If each customer is small maybe you need a huge number to make a decent business?

The table below shows monthly and annual figures for 100, 500 and 1,000 customers. Using the mid point numbers for all the other operational metrics.

None of these are unicorn numbers. On the other hand in the context of SMB SaaS they are achievable. Even here in Scotland official statistics show that there are 359 thousand SMBs. Scaling further is great. This show that even 500 customers generates enough cash to make a real living.

To make this work you would need to find the funding to get you to 500. And manage your monthly cash burn within these margins. But it is possible. Working in the real world

These analyses are based on averages. There is no such thing as an average business. Every SaaS will be different. Even the “choice” between SMB and Enterprise is not real. Potential customers occupy a continuum. These rough and ready calculations can help guide you. And provide a bit of fun. They are no substitute for paying attention to the real details of your company.

I have put the assumptions and calculations I used to generate these numbers into a free Google sheet. You can access this and play with the numbers for your business if you like. Remember this is a simple sheet so you can produce strange effects like the one in Analysis 2 above. And even if your numbers look good you still need to make stuff happen. In the end metrics are just the voice of your business. What they say will depend on the specifics - customers, product, business model. What you do will depend on you listening and acting on what you hear. These figures are only indicators of the possible. Having worked through them I am convinced of three things:

For anyone involved in building SMB SaaS, don’t be distracted or discouraged. The business model works. Its success depends on delighting your customers so stop reading and get on with it.

The cackle and chat about a potential startup valuation bubble has risen again in 2016. I wrote 3 posts about this 10 months ago and I am not sure too much has changed. I still don’t know when there will be a correction or what the trigger will be. But there are clear risks and the outcomes are hard to predict.

This post is not going to pretend to be an analysis of the scene. Much smarter people than me are providing that insight. I just want to reflect on a few basics and some scenarios which seem to be missing from most of the commentary. First thing is to get real about the markets in which startup investing plays a part. The Big Short is an excellent book and no doubt a good movie. It is not a substitute for understanding. According to Fortune funding for VC backed startups was $128.7Bn in 2015. With a sharp fall in the final quarter). By contrast the falls in Wall Street alone in 2016 so far are valued at around $1Trillion. Add in China and other markets and that loss could be $5Trillion. Startup investing, even at epic levels, is a cork bobbing in the ocean of global markets. If we want to figure out what might happen next we need to think outside the closed world of the startup ecosystem. The same applies when we ask ourselves what the impact of a bust in startup valuations might look like. Movement in public markets creates pressure in both directions

Tom Tunguz is a reliable source of real data analysis in the SaaS world. This recent post points out that price falls in public markets create some downward pressure on late stage valuations.

However, market movements are not as simple as this. Investor returns from public markets and many other asset classes are at historic lows. As I pointed out last year this makes startups look like an attractive option. Mahesh Vellanki has reinforced this point here. Economic pressure on traditional investments drives startup values higher. By increasing the demand from large investors. Of course this would change if market drama turns into real economic crisis. Internal strains and pressures

Global markets are not going to be the immediate cause of a bust in the startup bubble. What about internal strains of the ecosystem? This is where most of the commentary focuses in both directions. Insiders offer a wide range of opinions. Including Jason Calacanis who believes that any bubble has already been deflated. In a controlled fashion without anyone noticing.

Maybe investors are not as much in control as this article implies. There are more opinions than Republican candidates. And this could be sign of internal strains. That might just lead to a bust from within the startup universe. What would the impacts look like?

As a founder the message is proceed with care. If you cash you will be in a strong position. Competition may weaken and talent could become easier and cheaper to hire. But it will take time to get out of the woods so husband your resources. And watch out for ultra lean competitors. There will be startups out there innovating with high skills and motivation but no money. Customer trust is everyone's responsibility

The big risk in this internal scenario is loss of customer trust. If high profile startups with strong consumer brands fail this will cause widespread damage. For example, imagine a cloud service that holds precious family photographs disappears. Or an accommodation service goes under and leaves people without accommodation for the holidays.

In these situations a high percentage of the media will be eager to blame “the cloud” and “the internet” and “ global companies that don’t pay tax”. Whatever the truth, the road will become much tougher for early stage SaaS. Could a startup bust go viral?

The level of startup investment is small compared to global markets. You might think the internal impacts are the end of the story. Not necessarily so. There are a couple of ways a fall in startup valuations could trigger wider consequences.

Quoted stock markets had an indifferent year in 2015. Even before the sharp falls that have kicked off this year. This lacklustre performance two big swings. On the downside oil, mining and other commodity related stocks. Falls there have been more than offset by rapid growth in the FANGs. Another corny acronym which stands for Facebook, Amazon, Netflix, Google. None of these companies has the most transparent financial disclosures. So it is tough to tell whether they have a high dependence on startups or not. On the other hand I know that a big part of the money flowing into startups is going out on marketing expenses. And a lot of those dollars go to Facebook and Google advertising. How vulnerable is the revenue growth of these companies? It would only take a small surprise to knock market confidence. Trust is not just for customers

The other factor in grown up markets will be the behaviour of large investors. Remember, the guys whop play with other people’s money. Public opinion is still hyper sensitive to any hint of mistreatment for small investors. A perception that losses in high risk startups are being offloaded will be a big issue. Small pension holders or taxpayers cannot foot the bill.

Crowdfunded investments could create a special case of risk. Equity crowdfunding is quite new in the US but has been around in the UK for a while. Regulation is light and risks are high. Stand up and be counted

Loss of trust either from customers or the wider public is a real possibility. It will present a massive challenge for fragile startup businesses. Trust can only be won back by consistent, authentic ethical behaviour. One of the things I love most about the startup ecosystem is the high standards of ethics. These are almost universal. The true test of such values will only come when they are under threat.

No-one knows whether or when a correction in startup valuations might happen. If it does you will need to be prepared to look after your own business. The wider effects could be no more than a ripple. Or not. Beware the signs of a gathering storm.

I need to admit something. I have a problem with pure sales people. I have met some real nice ones. But the model just doesn’t sit with me. I worked all my life in professional services. Built on the principle that you must do AND sell. No separation. It is true that my former firm did hire the occasional pure “sales” person. It never worked. Those people did not add value. And our professionals did not value them.

I like to think of services in the words of a good friend of mine “We are all selling a little bit.” Hairdressers, plumbers, accountants, bankers. All services where the sale depends on people as well as the service delivered. I have also had the experience of building global partnerships. Alliances between professional services and clients/ partners with strong and successful direct sales models. This mix never worked in the real world. Sales people are great at selling a product but not at delivering a service. For me this creates an inherent conflict in SaaS. One consequence is a negative reaction to the wall of advice out there on how to more, organise and reward SaaS sales teams. I specifically hate the word quota. With a vengeance. All this material seems to be driven by an inherent assumption. That the the model for direct sales in traditional software companies is not broken. The advice and recommendations and even the basic language have this imprint. They bear an uncanny resemblance to the words you will hear inside Oracle or HP or whoever. This led me to work on a post called something like “Why you will never need sales in SaaS.” I have had versions of this kicking around for a while. But I realise that nothing in any of them is helpful or constructive. So let me try a different approach. Some SaaS companies will end up with a product which is best for large enterprises, government organisations and the like. The buying process in these customers is complex. The culture is unique and often challenging. Such sales need real people to spend time with the customer. Logic says that hiring people to engage with these customers will be necessary. For some SaaS companies at least. In my career I have worked with some of the best services sales people in the world. As leader I have been in charge of teams of professionals across the world. Generating billions of dollars of revenue. What have I learned? Below are a handful of truths. Things that work. Or at least reduce the risk of failure. This is not a system of success. But I hope it will be helpful if you are trying to build a SaaS sales capability. It is not just a numbers game

The funnel analogy is common in sales. Feed enough leads into the top and revenue will flow from the other end. Inevitable. Hire more sales people and generate more leads. Growth will follow. If this doesn’t work for any reason tweak it. Improve conversion. Fire your team and find better sellers. Market to a bigger audience. Build more product features. Until you have the economics working.

Is this a real philosophy? Crunch enough data and you will have the answer to life, the universe and everything? Of course not.

Metrics are a great way of figuring out what works and what doesn’t. But real revenues only arise form quality relationships with real customers. In an enterprise environment those relationships are complex. They are also few in number (at least until you are SAP). If you are SaaS is for large companies you need a clear plan for each relationship. Who do you need to meet? How will the target make its decision? What is the purchasing process? And much more. It is a long slog. You will have to listen to every nuance in each meeting. Understand and respond to different problems and agendas. Find features and benefits that work for the whole audience. Pumping numbers through is not the answer. Quality not quantity will win. Who will be the real sales person for your SaaS?

Get a clear idea who will truly sell your product. In the early days it is always the founder(s). By definition the team selling are also doing. Why then jump straight to a “pure” sales person? What you need is someone who can persuade your customer to buy your SaaS. Not just someone who says they can sell anything.

The best professional services sales people I worked with had the right combination of three things. Skills and track record that were credible with the client. The right personal and cultural fit for the client’s way of working. Enough knowledge and patience to navigate the buying process. Remember what counts is not your sales process. It is your customers way of purchasing.

In an established business I had to find these people and allocate them to accounts. It was a combination of personal experience from working with them and instinct. Not always right. In a startup you don’t have this. Instead apply a principle from the other side of the equation. Build up a persona for your ideal sales person. Then go out and find people who match. Hiring is a real jungle

Sales are built on relationships. You need the right people. No matter how big your company gets. No matter how tough the economy is. Finding the right people is always tough. Get over it. And be patient. I said it in a different context last week. Maybe means NO. You will still make mistakes. But only hire when your gut tells you it is right. This applies to sales as much as any other role.

My firm went through a big hiring exercise a few years ago. We needed senior people. Partners who would generate real revenue. Headhunters told us to expect an attrition rate of 20%. We achieved 6% over 5 years. There was no process. All we did was have people in the team meet candidates. If anyone who met them was unsure we said No. We kept going until we were sure. Every time. Don't be afraid to promote from within

Your best option may already be on the payroll. I can already see this happening with a couple of the SaaS startups I work with. Youngsters who have started as interns are growing before the founders eyes. Take a chance on someone you know. Who fits into the team culture. And has worked for it. This is much lower risk than insisting on someone who has a CV that ticks every single box.

Seeing people grow and succeed. In roles they would never have imagined a year or two earlier. This is one of the most rewarding experiences you will ever have as a leader. The fallacy of reward

Sales theory is often based on a pure, individual financial incentives. You pay on personal performance. You match or exceed the going rate. You hold individuals accountable and fire them if they fail. This is great for getting hard driving mercenaries. And high staff turnover. It is bulls**t for your business and your customers.

The more complex your SaaS and your customer’s business, the wronger it becomes. Selling products or services to large enterprises requires a team effort. Everyone from the PA who makes the appointments to the CEO who seals the deal has a role to play.

Startups are small teams by definition. Everyone and everything depends on everyone and everything else. The last thing you need in your culture is a high paid outsider. Motivated only for him or her self. Ditch those individual quotas. Get everyone working as a team in development and in sales. Reward team success. You will be more effective and have more fun. The myth of CRM

CRM must be the wrongest named software category in history. It implies that the system is about managing customer relations. In reality CRM is about building and tracking sales funnels and pipelines. Nothing wrong with that but call it what it is.

The wrongness doesn’t stop there. CRM is a crowded space with hundreds of companies - most SaaS based - offering solutions. The basic proposition is the same. A system and the metrics it drives will transform your SaaS growth. The trouble is sales is tough. And overcoming the challenge is not just about process and numbers. It needs thought, analysis, effort and a bit of luck. In the early days your success is not about being more organised. Or a more precise measure of progress. It will be about working out and guessing the right path. Through the messy world of the right corporate customer. There will be a tiny number of real quality leads. You will not win by trying to impose a pattern on these. Rather you must treat them as individuals until you see something that repeats. This will take a long time in the enterprise. The right choice at the right time

In enterprise SaaS sales the biggest decision is right at the start. Are we selling to the right customer? Most times this is followed by the other key choice. Are we selling the right thing to this customer? These things are true in every business. They matter more in enterprise sales. Because the time and cost of investing in a sales relationship with the wrong customer is so high. It can be enough to kill and early stage SaaS company.

The second choice (what to sell) is not about changing your product. It is about focus on the benefits that will make the biggest difference. Do not allow CRM or logo blindness to distract you from this fundamental. Dig deep to find out if you can add real value to your target customer. Listen to every contact. Direct or indirect. Even if your product is what they need, are they ready to adopt it and realise the benefits. Every culture is different

The sales model I have disparaged throughout this post does work in some places. National cultures vary. Industry cultures vary. Every large organisation has a culture all its own. You will build your own culture for your own organisation. Whether you like it or not. Once your SaaS is established it will have a culture.

You should respect and grow that culture. But you must understand and adapt to the culture of your customer. In enterprise sales buying is a reflection of culture and process. You will need to navigate both. I had a period where I looked after relationships with the Europe, Middle East and Africa (EMEA) business of two Fortune 50 clients of my firm. We were trying to sell the same portfolio of services to these clients. Their total procurement spend was similar - $14Bn per annum for one and $12Bn per annum for the other. As far as we could see the spend on professional services was also close. Yet the experience was different. There were many reasons. The first signal lay in procurement itself. One client had 180 people for its entire global spend. The other had 1,100 just for EMEA. At the same time, the buyers in the first client were happier to spend time with us than for the second. Despite having one tenth the resources. If you must hire sales people....

There are a series of process mistakes that are common in sales. Quotas too high. Measuring and rewarding the wrong behaviour. Hiring the wrong people. And so on. In enterprise SaaS you need to think deeper and more strategic. Fixing the wrong system is not the answer.

If your SaaS needs a sales force it is because your customer wants and need personal relationships before they buy. This is true for most large organisations. And it may be true for some things in the SMB sector as well. Professional advice is a great example. This is a great opportunity to learn about your customers and deliver real value. Instead of “How do I create the right sales process?’ Ask yourself “How can I best learn about my customer’s business and help them improve?” Build your sales team on that answer. Being in front of customers talking about their problems is fun. The rest is bull. Happy New Year to everyone. I hope you are ready launch into another SaaS year. I have spent a fair bit of time over the holidays thinking about some of the big topics related to SaaS. You will hear much more about my ideas over the coming months. For this first blog of 2016, I want to concentrate on one specific topic. Cash. Every SaaS is looking for moneyWhen I look at the SaaS companies I advise and/or invest in, almost all have one common feature. They have either raised funds in the recent past or they are planning to raise in 2016. In some cases both! So I was thinking about why SaaS businesses always seem to need money. And I came across this post from Jason Lemkin - Why Can’t SaaS Just Mint Cash? Here is one of the gurus of SaaS looking at the exact question. How come even successful SaaS needs more and more money to sustain progress? It also reminded me of an earlier post by another legend, Tom Tunguz. One of his themes is to analyse the published number of listed US SaaS companies. I think he has a basket of 51 that he tracks. This article highlights numbers for that group of SaaS companies. Almost none of these businesses are generating free cash flow or GAAP profits. Only 18 (of 48 at the time of the post) have ever recorded even 1 year with positive net income. The cash position is better but it still takes on average 6 years for SaaS to become cash positive. Why does SaaS eat cash?Why should this be? And does the SaaS business model still make sense if the overall economics are so tough? I believe it does because these numbers are a product of growth. Not the result of a fundamental flaw. That does not mean you can relax if your SaaS is swallowing cash. Growth is one factor but it can also highlight areas of the business model that need attention. The key challenges that create cash burn are:

Is Enterprise the only answer?One option to work your way out of the cash bind is to go up market. Enterprise sales generate more cash. Big organisations are great for upset. More users. New modules. Extra locations. It all adds up to a strong ongoing revenue stream. This option is not open to everyone. Selling to the enterprise means a substantial investment in sales and service capability. You will get the cash flow right in time. But only if you can raise more cash up front. $100m plus rounds are common in the US. This type of funding is much harder in other startup ecosystems. 4 SMB SaaS ideas for 2016And maybe that is not how you want to run your SaaS business. Your product and market may be squarely in the SMB sector. In this case spending heavy to hire sales people and sell to multi nationals would be the wrong strategy.

So we are back to the start. Every SaaS business needs cash. 2016 could be a year when the business environment gets tough. Fundraising may soon be harder than ever. If you are growing an SMB SaaS business, what can you do to mitigate the cash burn? I have no easy answers. These 4 ideas are worth trying:

Don’t be afraid to invest in what works. When you find a model. Or a channel. Or a person. Back them. One thing for sure. You will never succeed if you don’t spend the money you do have. Find the right solutions and go for it. |

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016