What the experts sayI read a great post from AdEspresso recently. Its about churn in SaaS startups that are selling to SMEs. In simple terms, high churn in the first 3 months of use is just part of the sales funnel. 5% churn or higher will not kill the business. Once through this early period, users will stick around. I work with a lot of SaaS companies and most of them target the SME market. This got me thinking about the economics of these businesses. I started to look again at the best SaaS sources. Tom Tunguz, Jason Lemkin, David Skok and others have written a great body of work on SaaS metrics. But it is all about selling to the enterprise. They talk about CLV or annual revenues in the 10’s even 100’s of thousands of dollars. The main element of customer acquisition strategy is people. Marketing, sales and customer success teams. Look at this post on the fundamental unit of growth for example. This is not the same world that many startups live in. This took me back to what has helped SaaS companies succeed in the SME world. The first thing I noticed is that the basic framework of SaaS metrics remains the same. Customer Acquisition Cost (CAC), Growth, Monthly Recurring Revenue (MRR), Customer Lifetime Value (CLV) and Churn. It is only when you dig into these numbers that the differences emerge. Customer Acquisition Strategy is the first differenceStart with CAC. Accepted wisdom is that sales efficiency (CLV/CAC) runs around 0.8. Anything over 1.0 is considered good and 2.0 is best in class. Coupled with high churn, this level of cost makes selling to SMEs look very unattractive. But this is not the reality. SME SaaS can achieve sales efficiency ratios of 5 or even 10. It just costs less to get a new revenue dollar.  There is a simple reason for this difference. Enterprise SaaS requires sales teams. Tom Tunguz post above lists Sales Development Reps, Account Executives, Customer Success Managers and Upsell Reps. SMEs need none of this apparatus. In fact they hate it. Small business owners are far too busy to spend time talking to reps. Once they have a a product they just want it to work. They don’t expect or want regular account calls. The recurring revenue model does not depend on direct sales. This doesn’t mean marketing, sales and support don’t matter. It does mean that the product and onboarding process needs to be friction free. Most of your customer acquisition will be online. So you need to learn what works. How you reach the right online audience and how you convert with minimal intervention. Partnerships or integration with parallel products can also be part of the mix. Keeping CAC low and Sales Efficiency high is an art form. CLV is linked to the recurring revenue modelCLV is another major difference. For an SME this number will be much lower than for an enterprise. The revenue models are different. At its most basic this means you need more customers to make a viable business. With SMEs there will also be much less opportunity for upsell. Service revenues from installation will tend to be nil. Growing CLV means you need to keep customers loyal. You need to embed your SaaS product in the life of their business. Be too good for anyone to risk a change. ...and finally churnThat brings us back to the final element as pointed out by AdEspresso. Churn rates can look high. The idea is that this is part of the sales funnel. It should be combined with conversion rates. The success of early months for an SME customer also depends on the onboarding process. Remember this is unlikely to generate much if any revenue. Yet managing your customers through this process is critical. Building a frictionless product is half the battle. Investing in people to help your customers will also pay dividends. Far more than a sales force. Onboarding is the secret of successWhat is the secret of a a great on boarding process? Des Traynor from Intercom wrote recently about the evolution of onboarding. In today’s world there is one key - change. You want the small business owner to adopt your product. He or she needs to change something. It can be a change in business process. A change in time allocation. Even a change in lifestyle. Your on boarding process needs to help your customer change. It also need to link that change to success for their business. To find out more about SaaS metrics and to receive a free copy of my SaaS Revenue model tool, subscribe below.

Comments

Late last year I started digging into the startup financial model. My whole career has been about how a business works. I don’t do blue sky strategy. I am not a system and process ops guy. I design, analyse and improve business models. This is the systematic view that works in my curious brain. I find myself poking around in a lot of different ideas. When I can see what works, I can help fix most things. SaaS is the leading business modelIn the startup world most things come back to software as a service (SaaS). Most of the businesses I am trying to help are SaaS based business models. The best startup ideas I see are SaaS based. The mechanics of the SaaS business model make sense. SaaS Metrics and the startup financial model hang together well. I have learned a whole lot about SaaS by working with some great companies. I read and follow a bunch of great people who share interesting stuff. (You can go here for my quick guide to the best SaaS reading). Revenue Models don't add upOver time though I have realised that there are some things which don’t quite add up. For example the sales model, some aspects of the economics, typical customer revenues. The experts view doesn't fit with my experience of real startups. I couldn’t make sense of this. Then it struck me when I was reading a post from AdEspresso. All the great stuff I read online is about SaaS companies that sell to the enterprise. But the companies I talk to are aiming at SME customers. How are SMEs different?So I started to think about why selling SaaS products to SMEs might be different. If so, what would that mean? This feels like it might be a long journey but here is what I have found so far:

SMEs want to take advantage of new digital technologies. There is a great small business market out there for SaaS companies.  Helping small business changeAt the heart of any successful business software is change. Adopting any software product requires business change. In a big organisation there will be managers and consultants to drive this. For an SME change is much harder. It takes time and focus. It risks the precious business that the owner has spent so long building up. You need to take away the pain as far as possible. You need to provide the encouragement and show the benefits. I would love to learnI want to help great SaaS companies serve the SME market. I love consulting for startups. Helping find the right growth tools. I am fascinated by SaaS customer acquisition strategy. I understand the revenue models. How can those SaaS metrics work better when selling to SMEs? What kind of small business consulting and advice do startups need?

I would love to hear from startups, entrepreneurs, growth hackers or customers. What are your ideas about how best to tackle SaaS for SMEs. Let me know your thoughts in the comments below. Or subscribe to my newsletter and receive my SaaS Revenue Model absolutely free.  Part 3: What will be the wider impact of a bust in startup valuations? Scroll down for parts 1 and 2. A quick reminder. Private investment dominates the current boom in startup funding. Public traded stocks play a much smaller role than in the past. For example in the dotcom bubble most big companies went to IPO. One point of view is that this will contain the impact. A lot of private investors will lose money. But the fallout for the general economy will be small. I don’t think this will happen. I will explain at the end why this will be a good thing. But warning this next bit is a real downer. “There are some things you learn best in calm, and some in storm” Playing for High StakesFor a start there is just too much money involved. Mattermark identified more than $100 Billion of US investment over 10 years. This only covers rounds over $100 million. Globally the numbers are huge. The private investment factor amplifies the pain of losing. There is no liquidity in private markets. Investors cannot bail out if they see the downturn coming. Or even after it has hit. No-one can cut their losses and run into safe havens. Mark Cuban made this point in a recent post. Startups are not a portfolioA bigger factor is the herd mentality. Most other assets classes offer shocking performance. Big institutional investors are counting on startup investments to beef up their total returns. Much of the money derives from the same sources that piled into sub prime and the like. The problem is that institutional investment tends to adopt a herd mentality. It doesn’t matter if they are right or wrong. Too many investment adopt the same strategy. This makes the whole system vulnerable to shocks. This factor is also amplified. In this case by a misunderstanding of portfolio risk. You will see a lot of advice about the risk of investing in early stage companies. Invest in a large number of opportunities and the big winners will offset the wipeouts. Build a portfolio they say. This is not a portfolio. This is a buying a lot of tickets for the lottery. It may well work and it has for many funds. But it is not spreading risk. Every investment just adds another high risk. Pick enough and one will pay off is the theory. The problem arises when the lottery stops paying out. There is no balance in the portfolio. Everything turns bad. Remember this is how it will be. Even the big quoted companies destined to join the corporate elite will experience large falls in value. Its not just about the moneyLets not forget that it is not all about finance. A downturn in startups will also have wide impacts because this stuff matters. People and businesses rely on the software startups produce. The network feeds itself and consumers love it when it does. Enterprises are creating massive value by using mobile and digital to do business better. Mobile money, mobile health and green startups are changing the world. If some of these companies fail, people will care. Big knock on effects are possible. Many apps interconnect through APIs. Your business does not just depend on the software you have. Other applications and data sources are integrated. Sometimes these are invisible to the user. Consumers are in the same position. A Matrix of Possible OutcomesSo what will the impact look like? This is harder to understand. We understand how a big bust in public markets transmits to the wider economy. Because this is a bit different, the mechanism is less well understood. In reality we don’t know. What follows is educated speculation. I have not attempted a systemic analysis just picked out some specific possibilities.

Green ShootsBut the tech industry will emerge stronger and better from everything that happens. A startup valuation bust will be a beautiful thing for entrepreneurs as I wrote in part 1. It will also be great for the whole ecosystem. A downturn is a real opportunity for innovation. The best ideas emerge from the furnace of hard times.

New HorizonsThere will also be big opportunities for individual entrepreneurs and investors. Remember two basic principles:

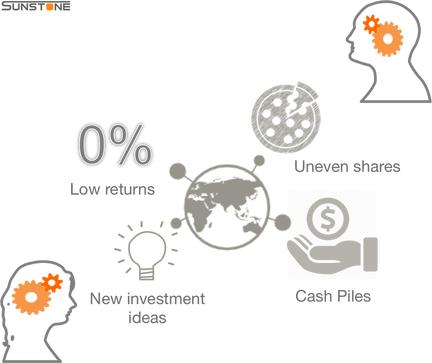

The startup ecosystem will shrink a bit. Those who are left will be the people with real vision and passion. A few years after the bust the industry that emerges will be bigger stronger and better than ever before. Writing these articles has reminded me I love startups. A real focus on change for the better and a great ecosystem of people to work with. These basics will not change if times get tough. I like to share the latest ideas for building a great business. If you would like these direct to your inbox, subscribe below. Thanks for bearing with me through this series.  This is part two of a series of three articles on the impact of a bust in startup valuations. For part one read down below. For part three…be patient. Valuations and the real economyMattermark published a fascinating blog post in January. It explores the connection start up investment and US interest rates. Do historic low rates fuel explosive growth in funding? The article explores various trend correlations which support some basic economics. Extreme low yields (zero in the case of interest rates) will give a high nominal price. For any stream of earnings. Fred Wilson of Union Square Ventures explained the theory in depth in March 2014. 0% Interest drives high startup valuationsThis essential fact lies behind one of 3 megatrends. Together these have created the current funding landscape. Another way of looking at the first trend is to consider alternative forms of investment. Look at four major traditional options. Public equity markets, public debt markets, property and physical assets, and business investment. Returns on the first two categories are at historic lows. Debt markets are flooded by Government debt. Real interest rates have turned negative in many countries. Stock Market Indices are high but this reflects a lot of money chasing a small pool of return. P/E ratios are also in record high territory. The picture for property appears more mixed. This is because the focus tends to be on capital values. But the explanation for the rapid recovery of property values is the same. It is a reflection of diminishing returns. I admit that this trend is patchy with a heavy concentration in narrow markets. Think London and Silicon Valley. Cash is piling upBusiness investment is a window on two of our megatrends. In most developed economies, levels of business investment remain low. Business owners are refusing to invest because the returns are too low. Many corporations have huge piles of cash on their balance sheets. But they are not spending. The supply of cash is growing at an amazing rate. The US, UK and Japan have all printed epic amounts of money in the last 5 years. The US is now calling a halt (or at least a pause) but the EU is just about to start.  This cash is not distributed in a broad or deep spectrum. The mechanism of QE is not a direct one. As a result, most of the printed money is sitting in 3 places. Corporate balance sheets. Sovereign wealth funds from commodity producing countries. And non banking financial institutions. Policy and regulation are keeping banks starved of funds. At the same time both private and public investment vehicles are awash. Little or nothing is trickling down to the bottom of the pyramid. Thomas Piketty’s treatise on inequality is a thorough reflection of this trend. New investment opportunities emergeA huge increase in cash concentrated in few hands. Historic low returns on many forms of investment. These trends create the conditions for massive investment in new structures and forms. This is exactly what we see. Our third megatrend is the current startup funding world itself. It is different from previous booms. Money is being invested through private vehicles. Much of the cash is institutional, corporate or from wealthy individuals. But it is hidden from the public markets. This means there is no liquidity. Investors cannot retrieve their cash. As Mark Cuban points out in this post, a fall in valuations of investments with no liquidity will be very painful. Where will the signal come from...This was going to be two articles about the impact of a correction in startup valuations. "Why the startup funding bust will be a beautiful thing” looked at the impact of a bust on startups. Part three will look at the wider economic and social changes a bust might bring. When I started writing I discovered that I needed this bit as well. Context is important. Changes in the direction of these trends will be the signal for the correction. When this signal is sent and how long it takes to transmit are big unknowns. In one view it could take a long time. In Europe the situation looks just like Japan 30 years ago. That has not unravelled yet. This applies to all Europe not just the Eurozone. The UK happens to be ahead but... We live in a dangerous worldOn a different view a dramatic turn could happen fast. The current fall in the oil price might be that early signal. Severe disruption caused by political factors is also a live possibility. Public statements from politicians and the media are depressing. In proper democracies are led by people who appear to understand nothing. Public discourse about the challenges on the borders of Russia or in the Middle East is verging on puerile. To describe most media coverage as First Grade level would be an exaggerated compliment. Other possible flashpoints - West Africa, the Horn of Africa, Korea/Japan, SE Asia. Not even on the radar. Startups could cause their own downfallWe must also acknowledge that startup ecosystem could be the cause of its own bust. People have come to rely on software in both personal and business lives. Many apps are interconnected in a web of APIs and integrations. A severe failure in the wrong place could cause massive disruption. Loss of trust and faith would cause investors to hold back. Valuations would fall.

Failure is not the only possible problem. There is a whole industry of naysayers just waiting to jump on a privacy breach. Security and integrity are vital to all our futures. Even a small problem could be magnified in the wrong circumstances. Again the issue is loss of trust and faith. Investment depends on sentiment as well as spreadsheets. Watch with interest. Tech start ups live in a global economy. It is one of the benefits of the digital revolution. That brings responsibility. Everyone in the ecosystem needs to pay attention to global trends. I am not an economist or an “expert”. My view could be way off. But there will be a down turn. I would love to hear what innovators and entrepreneurs think could be the cause.  Map of the South Sea Bubble c1720 One thing is certainThis week has seen a several interesting posts about money. Authors highlight the unusual funding structure of the current startup boom. The basic point is that most of the money invested is private. Many entrepreneurs and early investors prefer to avoid the public capital markets altogether. This Quora answer from Keith Rabois explains why the IPO is out of fashion. The result is large funding rounds for mature companies with established revenues. But the risks of this type of investment are much greater than listing on the stock exchange. Bill Gurley set this out in his article. It also means that investors money is tied up for long periods. Institutional Investor claims that VC funds now have a life expectancy of 14 years. The normal planned exit is after 10. Huge flows of money have resulted in fast rising valuations for start ups. There is plenty of speculation that we are seeing a repeat of the Internet 1.0 bubble. One thing is certain. There will be a correction. That is the logic of markets. Whatever the "fundamentals" prices will fall at some point. This raises two interesting questions: 1. Who will lose out and what might be the wider economic impacts? 2. What changes will startup entrepreneurs and teams experience? I will try to answer the first question in a future column. This one is about question 2. The money switch tripsThe fund raising environment will change. This is pretty obvious and it will be the first thing most people notice. Meetings with investors will become rare. VCs will announce they are “changing their investment strategy.” AngelList’s homepage will display far more pitches with much less progress. Talk about lack of deal flow will stop. This switch will flick overnight. When it happens do not deceive yourself. The money will not come back for a long time. Trailing round chasing the vanishing puddle of cash will be a mug’s game. The ecosystem evolvesOf course the startup ecosystem is not just about money. There is a lot of other support around. Incubators and accelerators, Universities, public bodies, mentors and advisors. All are investing time, expertise and sometimes a bit of cash. A downturn in valuations will show you who is making a strategic choice. And who is just jumping on the bandwagon. Advisors will be the first to disappear. Professional services is an industry that has to chase short term cash. Not everyone will walk away but many will. Mentors will split. Those who have committed will double their efforts. Others who are just exercising their egos will stop taking calls. I just hope that Universities and public bodies will stay in the game. If Government investment is worth anything it must be for the long term. The number of incubators and accelerators will shrink. The survivors will only focus on real business quality. Hubs built around creating great pitches and raising funds will not make the cut. Culture shiftsStartup culture will experience a more subtle change. Today it takes a lot of determination and resilience to be a successful entrepreneur. The challenge will multiply in a downturn. Lots of startups are nurturing. Many try to live real values and ethics. The investor spotlight will turn on the perceived costs of these attitudes. The great businesses will not be tempted to change. Strong and sustainable culture is essential to long term success. One big risk as the culture shifts. Diversity is already low but could be a major casualty. Women, minorities and those from less blue chip schools or family backgrounds could easily lose out. To everyone, don’t let this happen. Please. Cash is King...The work and social environment will change fast. You will feel it immediately and most of those feelings will be negative. But none of these changes matters that much to a startup. The big one is cash crunch. The harsh reality of commerce will reassert itself. No money, no business. ...long live the KingReduce burn, get cash positive or die. At the same time keep margins rising and aim for higher growth. This will be the day to day operating environment. The pressure will increase as investors feel the pain. Angels and VCs will demand cash distributions. Dividends, interest, loan repayments. Only the very strongest will survive. They will share three things:

And beauty came like the setting sun:There is no way of writing this that does not sound negative and scary. There will be a lot of casualties and not all will deserve to fall by the wayside. But the outcome will be beautiful.

When the sun rises the landscape will be clear and simple. The tech industry will have created the next generation of greats. They will not be unicorns. They will be the companies that made it into the ark. That worked as teams and maintained their values. The ones that will change the world. How can you build a great business that will have the strength to survive? What advice would you give to an entrepreneur when the easy money dries up? |

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016