do. Even when you are right. We all know that we need the ability to understand and maybe adopt different points of view. Easy to say but not so simple to execute.

Yet people do it. It is a natural process. This is how teams work when they work well. A group of people with a common goal but different approaches, skills and experience. When it is harnessed it is the most powerful human engine. Any theory of early man will tell you this is how our species survived. Subsistence hunting in teams. Get it wrong of course and conflict and stress are the result. Team building is a separate subject. The challenge of looking at things from many angles is the subject of Six Thinking Hats by Edward De Bono. What is it?

De Bono is famous as a kind of alternative philosopher of business. He uses psychology and human behavioural science to construct ways of tackling business strategies and problems. His work is about how you think rather than what you should do. Perhaps his most famous book, Lateral Thinking is a classic. A unique approach sets him apart from other leading thinkers.

Six Thinking Hats has also become a staple of the corporate library. It is described as a self help book on many lists. But it is the basis of many workshops, brainstorms and strategy sessions. It can stand alone or integrate into a wider learning and development programme. I have even seen it used as an icebreaker to help people get to know each other. The basic idea is that humans are capable of six different modes of thinking about a question or a problem. By putting on a different hat for each mode we can encourage the full range of perspectives on a question. Each hat is a different colour to distinguish it in our minds and in practical exercises. Effective use of the hats will give a complete and rounded view of the problem. More important de Bono argues that it will also spark innovation. All six modes of thinking can provide the new angle that illuminates the solution. Key Takeaways

Let’s look at the ways a startup might use each of the 6 hats:

Blue, Managing - This is traditional structured, task focused thinking. The standard modus operandi expected in large enterprises. Although not many people behave this way in practice. As a startup, don’t be afraid to adopt this mindset. Your world may feel random but the effort of ordering your thoughts can produce results. It may not be the first thing that strikes you. When you are swamped by data and options though it may be the best. White, Information - In this mode you deal only in known, hard facts. In a startup these are often few and far between. But it is vital to know what you do know. Confusing what you think with what you know has led to many errors and missteps. Your judgement will improve when you separate fact from assumption. And deduction (or just guesses!). On occasion reducing things to the bare facts will also make the way forward clear as crystal. Red, Emotions - The exact opposite of Whit. What is your gut reaction? What makes you want to laugh, cry or scream? Bring your passion to solving problems. This is often the default mode for a startup. But it can slip away as the reality of running a business bites. Don’t forget it. Black, Discernment - Not a great description. The author means risk averse, cautious and conservative thinking. Analyse the threats. Ask what can go wrong, what should you avoid. By convention startups embrace risk. This does not mean you should ignore it. Thinking through the downsides will help cover your bases. And be prepared if the worst happens. Solving a problem in a way which evades or minimises risk may also be the best answer. Yellow, Optimistic Response - Again the opposite of Black. Keep in mind that things might just be good. Or great. How could things take off? What would life be like in an ideal world? Do you have the resources to cope with explosive growth? If you hit the jackpot, what comes next? This is the thinking a startup can use to inspire the team and the world. Green, Creativity - The hardest hat to define. Think the unthinkable. Think different. Even if things are going well, could they be better? Turn your product into music. Make your software into a spoon. Whatever. Most startups are rooted in some level of creative, maybe crazy thinking. Like optimism this attitude can disappear early. Beaten down by the challenges of execution and survival. Keep going back to it and opening your mind. The beauty of the 6 hats is that it is a simple, easy to grasp model for a complex concept. There are lots of ways to use the model Any time you are struggling with a problem. Or trying to develop a plan. Come back to this it may help. It is not an every day habit. Too formal and time consuming. Startups should consider this approach in three main situations:

The Not So Useful Stuff

De Bono has distilled complex thinking and deep ideas into a clear conceptual framework. The Six Hats model is brilliant in its simplicity. Unfortunately he has written a book that wraps it back up in some abstract language. It is not the easiest read but it is worth taking time to understand his model. There are plenty of guides and tools if the whole book is too tough for you. Once you get it in your head, the framework is excellent.

I would add a seventh hat. It would be called “Put Yourself In Your Customer's Shoes” and the colour would be gold. If you can understand how your customer thinks you have achieved the gold standard for a startup. Or for any business. Of course hat 7 does not fit with the science and logic behind the original book. And your customers could be wearing any or all of the original six hats when they respond to your product. So perhaps number 7 is a summary rather than integral to the model. A startup should aim to find the customer’s perspective in any case. Next Steps

The fundamental concept of Six Hats is good. It has great value for a startup. Understand that there is no single right way to think about a problem. People approach things from different angles. Different perspectives are the fuel of innovation. They also help catch and avoid mistakes.

Use the 6 hats to approach complex problems. Or to reflect on progress and help make better plans. But don’t forget the seventh hat! For more ideas to help grow and develop your SaaS business, subscribe to our newsletter.

Comments

Benchmarks are a popular approach to business improvement. They provide an insight into how peers and competitors are performing. And identify areas for potential improvement. But they are an average. They highlight the status quo and undervalue innovation. The metric driven nature of SaaS makes it a great model for benchmarking. Think of this data as useful insight. You can learn from how others perform but don’t copy it. This is another in my series exploring how ideas used by large enterprises might be of value to startups. In this post I am going to explore Benchmarking. Benchmarking or comparison shopping is a popular technique. Many enterprises us it for business performance improvement. It is a big business in its own right. With a subscription model just like SaaS. Gartner and Hackett are built on benchmarking as a service. Every large consulting firm has offered the service at one time or another. The basic principle is simple:

Key TakeawaysThe potential to add value for a startup seems clear. Often founders have little or no data about the market they are entering or their competition. Limited networks and experience create open minds. But they are no substitute for experience of the sector or the business. Used well benchmarking can offer:

The Not So Useful StuffThis all sounds great. But in my experience benchmarking is no more than a way in. It provides an interesting snapshot but not a yardstick or a basis for measurement. I used to have a global client that spent millions every year on industry specific commissioned benchmarks. They cancelled after a few years because they could discern no performance improvement. There are several reasons for this. It is worth thinking about the following whenever you look at a benchmark or similar report.

Next StepsThere is an emerging industry in SaaS around benchmarks. The metric driven nature of the business model lends itself to this approach. I would suggest a startup pays little attention to this stuff. It is nice to see something and think you are doing better than the competition. But after the warm glow its adds no value.

The best way to view this is like an insider blog post. Useful background and a point of view but not the absolute truth. Learn from benchmarks but don’t copy them. If you are entering a market with established competitors it may be a handy way to learn about the competition. But don’t pay for it. Money is scarce and this will not be a good use. Focus on finding the metrics that drive growth and development in your startup. Work to improve on those measures and the competition will not be a problem. For more of the best business thinking for SaaS, subscribe to our newsletter.

I first found this book during a course on strategic thinking. Held at a delightful seaside resort in Denmark. One of the sessions included a film of Arie De Geus. De Geus was head of strategy for the oil giant Royal Dutch Shell in the 1970’s. During this time he adopted scenario planning as a standard. He described his experiences during the oil shock of 1974. When the price per barrel quadrupled almost overnight. He was able to pull a plan for a similar scenario off the shelf. And help his CEO respond faster and better to the crisis. It transformed Shell’s standing.

I was stunned. Here was a man who had thought the unthinkable. And planned for it. Remember this is long before Black Swans became a thing. Before PC technology disrupted the world. Amazing. I had to know more. When I returned home I went to a bookstore (yes this is before Amazon as well). And found a slim volume written by the Dutchman. The Living Company became my favourite business book. It is a classic in my opinion. Although not as well known as some of the works I have written about. And there is a twist. The message goes against one of the big founding myths of the startup world. It is about survival and sustainability. Not growth and fabulous valuations. What Is The Living Company

During and after his time at Shell De Geus studied some of the world’s largest companies. He started from a unique perspective. The average lifespan of a multinational is just 40 -50 years. Less than a human being. For example between 1970 and 1983, one third of the Fortune 500 ceased to exist. Bust or taken over.

He wrote an article for Harvard Business Review called the Learning Organisation. And then published The Living Company. Both have a single theme. What makes the survivors different? Long Term Business - Elephants Not Unicorns

The startup world today is like stock markets since the tulip mania of the 1600’s. It exalts the short term. The highest valuation or the most money raised today. Not yesterday and not tomorrow. We have even coined a word to describe these winners. The unicorns.

Yet the role models are Google, Apple and maybe Amazon. These look more like Elephants. Enormous, successful and long lived. Page, Brin, Job and Bezos did not start a business for the short term. They wanted to change the world. I believe there is far too much attention paid to funding and valuation. We live in a day trading kind of world. Startups are still high risk. Those that survive even for 20 years will build a real business. When the boom ends the companies left standing will not be just those that have raised the most money. If your aim is to be in that group, you can learn from The Living Company. 4 Lessons To Build Your Own Business

The book is not that long. But it is rich in examples and thought provoking angles. In the end there are 4 core lessons:

Sensitivity. Learn and adapt to the environment. Including markets, regulation and social expectations. Every startup needs to begin this way. You will not get off the ground if you don’t understand the market. Retaining that sensory perception and allowing to determine business strategy is a different matter. Pivots are a part of sensitivity. Over the longer term a company needs to keep listening. And be ready to undertake a total transformation. The digital revolution is going to find out many established organisations. It will destroy those who are not able to change in response to a new environment. There are also cautionary tales within tech. Look at the challenges facing Microsoft. It has been slow to react to the growth of mobile and the cloud. Identity. Great companies are communities with their own culture, personality, rituals and traditions. This emerges. It cannot be set from the top. I have seen great business dying a slow death. Because consultants and CEOs demand strategic change. And declare victory as the house of cards falls around them. Startups need to understand their own culture. This is a collective thing. It is not just the choice of the founders. But in the early days you can influence it. In ways that will not be possible once you start to scale. At all times you need to nurture and value your identity. Even including the parts that frustrate. Whatever the size of your business, the one tool you have which can impact identity is hiring and firing. I worked for many leaders during my time in business. the single most successful did not change strategy. Or organisation,. Or goals. He looked at the top 100 people. he fired the 5 who were the worst fit. (note not the worst performing). And hired 5 new people. In less than a year performance improved by 20%. As a startup, hire people. Check experience and qualifications. And pick those you want as part of the team. Nowhere is this more true than when hiring sales teams. Tolerance. Long lasting companies work with their stakeholders. Governments, suppliers, customers, shareholders, teams, partners, communities, unions. Everyone and every group. They adapt to the ecology that surrounds them. Remember we are talking multinationals here. Tolerance also requires a decentralised approach. The ecology is different in different countries, markets or communities. Startups need to empower people to build and sustain relationships. It is great to be data driven. But numbers do not answer every question. Command and control delivers short term results. It does not make a business sticky or sustainable. The eco system is not just something you give back to. It is the life force that sustains you. This may prove the biggest challenge to today’s tech giants. Conservative Financing. Tis is definitely not part of today’s startup culture. In reality every entrepreneur needs to take some financial risk. But the long term financial strategy is not to keep multiplying that risk. Over time high financial risk will expose any company. The goal of investment is to get your company from nothing to a stable sustainable base. Becoming self financing is the object. Not reaching for an even higher valuation. Massive injections of funds to sustain cash and profit negative growth can only last so long. This is a statement of the obvious but it seems forgotten. Memory will return fast when the current investment cycle turns. Read the book and learn. There is something of value on every single one of its 238 pages. Start Your Own Business - Become An Impala

There is another lesson from The Living Company. Most founders are not starting the next Google. Or even a short term unicorn. So what. Mobile and digital are changing the way we work and do business forever. We are going to shift from a corporate dominated economy to a more diverse and fragmented structure. The future will be about making a living not just having a job.

The impala is the most common antelope in southern Africa. Around 150,000 in the Kruger National Park alone. Yet each individual is a beautiful, fragile survivor. And the species succeeds in large co-operative herds. This is the future we need to build. Not just start your own business. Help create large numbers of long term, sustainable businesses. None enormous. Working together to create communities and economies that help everyone live a better life. For regular updates on the best thinking about SaaS subscribe to our newsletter below.

Playing To Win is one of the best selling strategy books of recent years. It is intended as an example and method for large corporations. But it includes lessons about clarity, focus and honesty which apply to any business. Be careful though, Some of the thinking is dangerous for a startup

This column is a new diversion for me. A lot of my small business consulting is about applying knowledge. Over my career I have studied pretty much all the biggest business ideas. And I have applied them for the last 30 years. I use my practical experience of what works every day. But I have not found an effective way to share this in my writing. This is my latest attempt. I am going to make a brief explanation of a well known business idea. And then explain what a startup can learn from this thinking. What Is Playing To Win?

Playing To Win is an approach to strategy set out in a book of the same name. The book was co-written by A G Lafley, long time CEO of Proctor & Gamble. And a strategy consultant who advised him in that role, Roger Martin.

How Does It Work?

Key Takeaways

Lafley believes that business strategy is sound in theory but abstract in practice. Playing to Win (PTW) is a systematic attempt to explain how strategy applies in the real world of a global corporation. The book is built around examples from P&G during his first tenure as CEO. (He returned to the company for another stint shortly after the book was published). The case studies support a model with 5 major components:

Each of these elements requires careful planning and forceful execution. The stories in the book focus on how P&G delivered. How they achieved the clarity and consistency to make PTW work in practice. It is tough to have a big workforce pull in the same direction. Making strategy happen in large corporates is a complex challenge. P&G’s results during Lafley’s first time as CEO show a high degree of success.

A startup is different in almost every way from P&G. Yet PTW holds some value even for a company at the opposite end of the business spectrum.

Most important is clarity and focus. The diversions and complexity may be less than in a global enterprise. But many startups try to do too much. The key message of PTW is do some thinking and make some clear decisions. Like all strategy it is as much about what you don’t do as what you do. The structure also provides a useful way of thinking about business strategy. Set objectives and be clear about your markets. Define the differentiation that will allow you to succeed. A template based on the ideas in this book can be a helpful aide. Writing your plans down in this format will give your business plan added credibility. I also like the emphasis on honesty. You need to be clear eyed about what is unique in your business. And about the capability you require to build your startup. Be honest with yourself if you expect to appear authentic to your customers. The How To Win section of the book is strong in this respect. Even the largest consumer products company on earth does not have automatic differentiation. You don't need to articulate unique value from day one. Think about the path to competitive advantage. PTW frames strategy through some excellent questions. They are a good way into strategy for any business: “What qualitative evidence can support your winning aspiration?" “How can you write down the critical assumptions that create your where to play approach?" “What are the biggest challenges your customers/ potential customers face?"

The Not So Useful Stuff

PTW is like most business strategy books. The examples and illustrations come from established global leaders. These are interesting but hard to translate into a startup culture. Specifics about management roles and job titles for example are far too onerous for an early stage company.

There is also a big problem with some of the language and ideas. As the title implies there is much about beating the competition. I find fighting analogies unhelpful for startups. The startup world is not a zero sum game. The efforts of founders and the benefits of technology add to the economic sum. It is not about winners and losers. Business is not war. I know that some people find battle cries inspiring. It is a short term fix. Your startup needs to have a positive reason for existing. Even if that reason is just to make people a little happier by showing them pictures of cute cats. “We are better than the competition” is a negative outlook. Next Steps For Startup Strategy

Not every book on business strategy is worth reading. Playing To Win is an exception. It is short and easy to follow. Stories from A G Lafley are in separate sections so it is easy to focus on these. I will be sharing more tools and ideas from the business world. How can big business ideas help startups and SaaS companies grow and develop? If you want to know more, get in touch or subscribe to our newsletter for regular updates.

A startup I know well posed an interesting question this week. The company is raising seed funding. The founder has taken a cautious path so they have good traction and a revenue model. Nonetheless this is their first formal round. One of the potential investors is unsure of the valuation. Said investor is proposing a discounted cash flow (DCF) valuation.

DCF is a well known and respected technique. Analysts use it to value companies and long term projects every day. What is it? Wikipedia has this definition: In finance, discounted cash flow (DCF) analysis is a method of valuing a project, company, or asset using the concepts of the time value of money. All future cash flows are estimated and discounted by using cost of capital to give their present values (PVs). The sum of all future cash flows, both incoming and outgoing, is the net present value (NPV), which is taken as the value or price of the cash flows in question.

This is crazy

The investor who thinks this works for any startup is crazy. The basis of DCF is a forecast of future cash flows. Startups operate in a world of complete uncertainty. Forecasting revenues is near impossible. When I review startup business plans, I am interested in the financial forecast. But I am looking for messages about ambition, traction and product/ market fit. I don’t place any reliance on the actual numbers.

If you look closer you will see the little word “All”. Proper DCF uses all future cash flows. Most startup business plans only include 3 year forecasts. I have seen DCF valuations of capital projects that cover 20, 30 or even 50 years. At seed stage most startups do not even survive the 3 year horizon.

Kissing Cousins

Small Business Consulting Gets Technical

If you get this, it is easy to dismiss DCF. Irrelevant in the startup world. I agree that it makes no sense as a basis of valuation. But I think it does hold some lessons for a SaaS business. The reason? Consider the parallels with lifetime value (LTV).

LTV is one of the core SaaS measures. In concept it is just like DCF. You calculate the revenue or gross profit for each customer. Over the life of that customer. Your LTV is the sum of the future expected revenues from each customer. Then calculate an average to give an individual customer LTV. This is a newer and less developed way of measuring value compared to DCF. What lessons can we learn from LTV’s older, more grown up cousin?

“Discounted by using the cost of capital” covers several things. Including some reasons not to use DCF for a startup valuation. The words are bit of financial jargon. So the best way to illustrate this is by unbundling the terms.

Lifetime

On the surface LTV is better than DCF at estimating lifetime. In many calculations there is no fixed lifetime for DCF. Churn puts a time horizon into every LTV number. The maths of using churn this way makes sense. But it hides an important truth. Churn happens to the customers that leave. In every cohort there are customers that stay around. These accounts are gold mines.

Mobile network operators discovered this early. Your average customer is an expensive habit for an MNO. He or She changes the handset every 2 years. This means an extra customer acquisition cost. Often linked to a drop in monthly revenue. Some people don’t do this. They keep that old Nokia forever. Many love those things. The monthly line rental and the call package just keep rolling in. You can make an simple calculation of the impact of this. Take a typical SaaS SME customer paying £50 subscription every month. The company has nice ow churn of 1% per month. The average LTV formula is: LTV = MRR X 1/CR where MRR is monthly recurring revenue and CR is the churn rate. For our example customer this gives LTV of £2,500. The technical term for revenue which keeps going forever is perpetuity (P). The formula for calculating the value of a stream of payments in perpetuity is: P = MRR/IR where IR is the monthly interest rate or cost of capital if you have that number. Imagine an interest rate of 10% per annum. High by today’s standards. Above the range of 4-8% quoted in this article from Forbes last year. Using this rate P is £6,000. The customer you keep is worth almost 2 and a half times the average. Before you factor in the extra customer acquisition costs involved. Remember you have to replace every user who cancels a subscription.

Cost of Capital

Applying calculated values for cost of capital makes no sense in the startup world. The uncertainty overwhelms the logic. Thinking about how to approach this provides a great frame of reference for some big decisions.

Time value of money is real. A dollar today is worth more than a dollar in a year’s time. But the difference is not infinite. Discounts to encourage people to pay for a year or more upfront make sense. The cash upfront can be a lifeline for a startup. Dry interest rates don’t capture the value that represents. You do need to think about what works when pricing up your product. Capital structure is not a relevant factor. The startup parallel is opportunity cost. Or cost of choice if you prefer. Again not something to wrap up in a percentage rate. But think about adding features, tackling new markets and so on. Early doors the question is which option brings the best return. As you become established this changes. Now you need to ask a different question. Will investing in something new earn a good return? Is it better to put more resources into your proven business model? Weighing up risk is one for the future. Every step on the startup journey is high risk. A founder cannot be reckless but risk analysis can lead to paralysis. Be aware but don’t lose the bias to action.

Building a scalable SaaS recurring revenue model is neither art nor science. Skill and judgement play a part in every decision. A rigid set of rules and boundaries has little meaning. A framework that helps your team recognise the context of your choice can be a big help.

Professional finance managers have developed some great techniques. DCF has an important place in this arsenal. The basis of these models is valid theory and sound maths. The variables involved kill the benefit for a startup. Understanding how established methods work can still provide valuable lessons. The core SaaS concept of LTV is a cousin of DCF. Looking at both is illuminating. No two SaaS businesses will be the same. Within any business, the context of each decision will also be different. No advisor can lift the load of making tough decisions from an entrepreneur. Great small business consulting for a startup means helping founders make those choices better. Helping new leaders learn their craft. Subscribe for more insights direct to your inbox. Learn the Startup Craft to Build Your Revenue Model I had a great week. I met 7 startups I hadn’t seen before and caught up with four more. I heard from some great entrepreneurs. I saw some excellent ideas. I enjoyed real fun conversations. I also visited a new co-working space in Glasgow which was fantastic. You can see a picture of the Govan Workspace above. Congrats to Mike Hayes (@_MDHayes) and the team for setting it up. Most startups I meet are looking for funding or aiming for the next stage of growth. Every founder I saw had some kind of plan or pitch to share. Maturity MattersThe details of the plan vary with the maturity of the business. There is no fixed rule but investors expectations also change as your business grows. I have set out below my quick reckoner for the key points at each stage. Before that, I thought you might enjoy the product from one of the businesses I met this week. This link will take you to a living infographic from Stipso (@stipso). Stipso is an Edinburgh based company. They are aiming to transform the way data gathering works for marketing. They do this with a new kind of infographics. User engagement jumps when Stipso goes live in the real world. My thanks to Brian Corcoran and Steven Drost for letting me share one with you. The infographic does not show in some browsers (may fault) so click the button underneath of the screen below is blank. Enjoy. The 7 Ages"And one man in his time plays many parts, Napkin - First scribble your idea on the back of a napkin. The only person you need to convince is yourself. If I meet you at this stage, I will try to show you the risk and dangers of becoming an entrepreneur. Building a start up is hard so it is not for everyone. Accelerator - If you like your idea the next step is to start building something. You may choose to apply to an accelerator or a similar startup support programme. The biggest criteria for entry is the quality of the team. the only other thing that matters being different. Your idea or your company need to stand out from the crowd. Development - An accelerator (or just a few months hard work) will get you an early product. Maybe your first customers. Continuing development is likely to need funds. Now its time for seed funding, maybe through angel investors. You might be asked for quite a lot of detail at this stage. I am only looking for three things: a great team; some evidence of market traction; and a clear description of the business model. Follow on - Seed funding arrives after intense scrutiny by investors. Often accompanied by much stress for entrepreneurs. The investment basis is an over optimistic business plan. Soon you need follow on money. The main source will be the original seed investors. No-one wants you to fail at this stage. I need to see the same things with one extra. Some evidence of execution. Mistakes and over optimistic assumptions are fine. But I want to know you have used the money in a focused way. You have made real progress and you have learned from the things you have done. Growth - You establish product/ market fit. Then you build a repeatable, predictable growth engine. You are ready for growth. It is time for Series A (and B and so on). VCs and strategic investors get involved. Your numbers come under much closer scrutiny. Detailed market analysis and revenue forecasts supported by full financial projections are the order of the day. Team and traction are still essential. I also want to know precisely how you will spend the money and the results you expect to produce. Most of the cash should be on sales and marketing through proven channels. Scale - Deliver results from VC investment and you will be ready for an exit. This either an IPO or a sale to a strategic investor. In turn, a sale could be to a trade player or an investment fund. Information requirements are set by Regulations and industry practice. This is also the first point where valuation counts for me. I now have enough information. I can determine whether the price will yield an acceptable return on investment. Its not all plain sailingFund raising is an unpredictable process and issues can arise for lots of reasons. It is worth highlighting three common sources of tension:

No EscapeCorporate Planning - Even if your company is the next Microsoft or Google you will not escape. I admit that if you turn out to be Bill Gates or Larry Page you will be reviewing the plans. Not writing them. For normal mortals the corporate world means quarterly and annual planning cycles. As an investor I have no interest in this aspect of the rat race. As an advisor, I would say remember it is still a pitch. The corporate planning cycle is a way of allocating shareholder resources. Deciding which investments in people, assets, product or markets offer the best return.

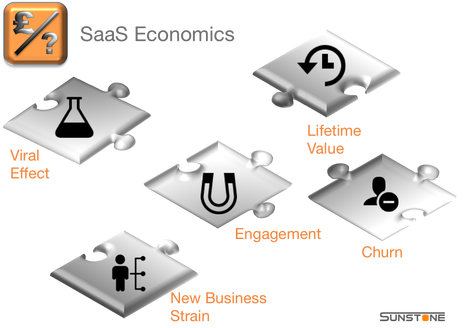

Which of the 7 Ages is your business? Let me know if you need any help or ideas.  The best SaaS business model thinkingThere is a lot out there about the economics of SaaS business models. Tom Tunguz publishes regular insights about the performance of listed SaaS companies. David Skok offers some excellent analysis. His blog describes the formulas and ratios that drive growth and profitability. SaaStr provides practical tips and advice that are valuable to any entrepreneur. You could build up a list of metrics from these sources that runs to 10 pages or more. I am not about to try to summarise all this great material in one blog post. This is not a guide to the economics of a SaaS business model. Reading great analysis and working with SaaS startups is a great way to learn. Some key ideas strike me as worth sharing. CLV is key to unit economicsSaaS is about unit economics. You can calculate a realistic customer lifetime value (CLV) from the available data. I wrote a detailed post on the subject a couple of months ago - find it here. CLV is the building block of long term value. It shows the route to sustainable profit. The formula for CLV includes direct cost and cost per acquisition. Your direct cost should take account of cost to serve. Few SaaS companies can just sign up a customer and watch the money roll in. Those awesome margins need to support a proper service framework. You must keep your users engaged. Every startup need to get to product/ market fit. At this stage SaaS companies are gaining paying customers with a repeatable process. The results of this process are also predictable. They can estimate the CLV of each customer. But they are not profitable. Now SaaS suffers from an old fashioned challenge. New Business Strain (NBS). New Business StrainNBS is an idea from the life insurance industry. In simple terms the cost of acquiring a customer is all incurred upfront. Value is realised over a period of years. Accounting and cash flow follow a more basic model. Growing a business means high short term CPA. This outweighs annual profits from recurring customers. You need more money than you are earning to keep growing. Financing this strain is the purpose of Series A investment and beyond. The alternative is slower growth. B2B is not viralConsumer business models can generate hyper growth and profits. This occurs when viral spread reduces CPA to near zero. This kind of viral growth is not open to B2B SaaS. Viral cycle times are much longer. Months not hours. When recommendations do happen they generate warm leads not direct sales. It may be slow and partial but viral still matters. Jason Lemkin wrote a great post about this. Over time, references from your customers will make a difference. Growth will multiply and CPA will come down. When this kicks in, NBS will shrink fast. It just takes time. ChurnLifetime is a key word in CLV. The number that determines L is churn. The value of your business is sensitive to tiny variations in churn. 2% per month gives a half life of 3 years. That is you will lose 50% of your current customers by the end of three years. Increase this to 3% and the half life reduces to just 2 years. Churn should be a small number. But your margin for error is tight. Engagement is the great unknownThe biggest gap I see in current SaaS thinking is engagement. Measuring the economics of engagement is hard. We have a crude measure for pre sales engagement. Conversion of leads into paying customers. We have another simple number for post sales engagement. Churn. The process between is more of an art than a science. Finding which steps in the process reduce conversion rates would generate immediate value. Fine tuning service and support to reduce churn will pay long term dividends. Concentrate on measuring behaviour first. If you can attach a numerical value great. Build the model specific to your business from the ground up. I am leading a workshop for a bunch of Scottish SaaS companies in early March. We will focus on one aspect of engagement. Looking forward to learning some best practice then. Benchmarks - handle with careSmart analysis of SaaS performance has led to some well constructed benchmarks. For example Annual Contract Value (ACV) to marketing cost ratio should be around 2:1. This shows a healthy level of NBS. Or Brad Feld's recent suggestion the rule of 40%. The sum of your net margin and your growth rate should be at least 40%. There are many other examples. All are rules of thumb suggested by experienced investors and entrepreneurs. Such benchmarks are due respect. But handle with care. General rules like this are a good indicator of progress but a bad way of setting goals. Think of benchmarks like a thermometer. They give a rough guide to general health. They are not a management tool. You would stay sick for a long time if doctors just focused on reducing your temperature.

I encourage you to read and follow some of the blogs suggested in this post. If you would like help building a SaaS model for your business, get in touch.  Well intentioned illusionsThe Startup world is home to many well intentioned illusions. One of these is the concept of "investor ready." This apparently attractive phrase is dangerous because it misleads about investor priorities, it misunderstands the relationship between investors and companies and it misrepresents the role of advisors. Let me explain. If you search the Internet you will find literally thousands of blogs and articles by angels, VCs and investors of all types setting out their investment priorities. Investor ready is never on the list. There is a very simple reason. Investors want to invest in a great business. The common factors - team, product/ market fit, growth potential etc - are all about being a great business. Investors and Startups need each otherInvestor ready also implies, even assumes in some cases, that Startups are supplicants aiming for the grace and favour of investors. This is wrong. Investing in a Startup is a partnership. The investor has scarce resources of money and expertise but the Startup also offers something rare, great people and an innovative business. Investors need Startups as much as Startups need investors. A few things you need to knowA mini industry has grown up around matching these needs. If you are a Startup looking for money, you will encounter this sector of the economy sooner or later. Here are a few things you need to know:

Hold onto your dreamThe most essential thing is not to lose yourself and your business in the “investor ready” process. I have seen many pitches and business plans (which is just another pitch remember) refined and improved by expert advisors which are designed to answer every question in the book. Unfortunately this never works. Once investors see the pitch sooner or later they will ask the question about the business fundamentals that is not in the book and the founder will be exposed. Your job in the investor ready process is just another pitch. It is not to change the market, the product or the revenue model to meet someone else’s expectation.

Securing investment is an exciting moment for any business. Remember you are an equal partner in that investment and what you bring is the idea and the passion. Lose these and the investment will be and for you and the investor. Keep them and we will all have fun. |

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016