|

The value of the biggest B2B SaaS companies has been growing. But not at the epic rates experienced by B2C software. At the same time, the number of B2B SaaS startups also keeps rising. Is there enough potential revenue in the market to justify the level of SaaS investment?

Jason Lemkin wrote a fascinating piece on SaaStr a couple of weeks ago about the SaaS Decacorns we need by 2021. His conclusions were optimistic. He believes both that the market as a whole is big enough. And that there are companies there with the potential to become the mega leaders of the future. I am not going to comment on the latter. But I share his optimism about the overall market. We are only scratching the surface of the opportunity for B2B SaaS. Reaching this potential demands great products which solve real business problems. SaaS companies must also help customers execute change to realise the benefits. All in the face of strong resistance from multiple vested interests. It will not be enough just to wait for the market to come to you. B2B SaaS companies need to take the lead in finding strategies to overcome these challenges. The scale of the opportunity

The simple fact is that traditional on premise, licence based revenues still account for the bulk of the enterprise software market. You can fill your boots with various projections and analyses of this topic. For starters check out this Forbes collection.

However you look at the numbers this makes no sense. SaaS is an ideal platform for innovation and increases the speed of change. It offers much greater flexibility and agility. Integration allows for rapid adoption of best in class. And its cheaper. The question is not whether the market opportunity exists. What bugs me is why progress is so slow. Executing change

The one word answer is change.

SaaS does not bring any of the benefits listed above to business. It provides a tool or a platform to improve a business. To realise the gains, the business must change. Businesses of any size find it hard to execute change. An established business is different from a startup in two major ways:

Organised resistance

Your customers internal opponents are not the only losers. Growing SaaS by a factor more than 20x will do damage to the traditional software business.

The big enterprise vendors are the tip of a large iceberg. They are the visible part of an ecosystem that includes consultants, systems integrators, lawyers, training providers, independent software vendors, project managers, change leaders, corporate IT careerists and a raft of other specialists who have carved out a niche that is built on SAP, Oracle and the rest. The strident voices of direct competitors are easy to deal with. Corridor whispers by trusted advisors and “independent” experts are much more insidious. So be careful. Resistance is everywhere. The Chairman's View

I share Jason’s optimism about the scale of the SaaS opportunity. That’s one of the reasons I love working with B2B SaaS companies. The winners will have great products and fantastic teams led by brilliant leaders. They will also have an effective strategy to overcome the barriers to change.

Each market opportunity and in some cases each deal will need different specifics. The outlines of any successful approach will include:

And do it all with confidence. The market is moving toward B2B SaaS. Let's help it along.

Comments

The Profitwell blog from Price Intelligence is often an interesting read. Rather than focus on outright promotion of their product, the team share the lessons learned from their customers. This bodes well for the future of that business. Listening to customers is a clear strong point. It also offers some genuine and surprising insights.

A couple of weeks ago Patrick turned his attention to SaaS benchmarks. The industry has developed accepted norms for certain numbers. Such as churn, expansion revenue and growth rate. These often quoted as essential thresholds to success for aspiring SaaS businesses to cross. Profit well also shows that they are all wrong. By big margins. This is the first of a series so you may want to sign up for future updates. You might also want to pause for a second and think about the purpose and value of benchmarks as a species. Who wants to be average?

By definition, benchmarks are an average of performance. Summed from a group of companies in an industry. Even the industry is defined by someone else. It may not be that close to the group of peers or competitors that you would choose.

This makes an interesting comparison but a terrible goal. Your ambition is to be a leader. The best product or business out there. Striving for average doesn’t cut it. Best practice v innovation and disruption

Benchmarks are a window into the past. They are a report of historic performance. And the individual definitions are also relics. Reflections of existing business customs, methods and practices. SaaS startups are out to disrupt these worlds. To use innovation to challenge and overturn the established order. The very stuff of benchmarks is irrelevant to this agenda.

Are these the best things for your business to measure?

In a fast growing SaaS company there is no shortage of potential metrics. The leadership challenge is selecting and focusing on the most important numbers for your business. Benchmarks chosen and defined by an external agency are unlikely to be the top of this list.

External numbers of this type pose another risk. The right metrics are the voice of your customer turned into data. Benchmarks are the amalgam of the voice of other people’s customers. I know which set of numbers I would rather listen to. How meaningful is SaaS benchmark data?

When you start out, benchmarks can be a useful to work out whether you idea is viable. You can use them as a rule of thumb estimate of profit potential for example.

Once you get beyond the back of an envelope stage, you need real data. It seems obvious that benchmarks can only be of value if they provide a reliable barometer. Profitwell shows that this is not the case for some common SaaS performance benchmarks. My experience tells me that more established data sources suffer the same problems. Remember that public benchmarking companies like Gartner, Forrester and IDC depend on the companies benchmarked as a source of revenue. When I have worked with these companies, they aim to be impartial and act with integrity. Yet they are still vulnerable. It reminds me of a conversation I once had with the sales director of a big insurance company. “If you want to know how independent our resellers are” he said to me “watch what happens if we double the sales commission on a product." In reality public benchmarking data is best used as a prop for sales pitches. Some people like that sort of thing I guess. As an operational tool, I am a serious sceptic. I recognise that estimating future performance or evaluating past performance is hard. More so in a startup. That is because of deep inherent uncertainty. Risk is both the worst and the best aspect of making business decisions. Don’t be fooled into trying to mitigate it through false and irrelevant numbers. And well done to Profitwell for challenging the consensus.

Negative churn is a bird in the hand that is worth less than two in the bush. It has emerged as a preferred and even promoted SaaS metric over the past couple of years. Yet by offsetting two (or even three) numbers against each other it obscures rather than illuminates business performance. Why would a goal that offsets two conflicting numbers be the right metric for your SaaS business?

To be clear, negative churn arises from two things 1. On the plus side, the increase in revenue from existing customers. 2. On the other side the loss of revenue from customers who stop using your SaaS (or churn for short). Thus “Negative churn” is the result of a sum, not a number or phenomenon in its own right. Setting this as a goal or celebrating it as an achievement creates an inherent conflict. Let’s start by examining the two faces of strife in turn. Customer or revenue churn?

The trigger for writing this blog was a post by one of my favourite SaaS companies, ChartMogul. How do I calculate LTV when I have negative churn? digs into the exact problems that this “accomplishment” generates. And the first issue centres around that single word churn.

Churn arises when a customer stops paying for your SaaS. At this point you are already losing two things: a customer and a monthly or annual revenue receipt. For an SMB SaaS these two numbers may give a similar message. The flat pricing structure and similar base limit dependence on key customers. But if you are winning larger customers? Then the monetary value of the revenue lost may not be an accurate reflection of the number that churn. Lincoln Murphy has explained this challenge well in SaaS churn: Measure customer or revenue retention. Lincoln believes the focus should be on the dollar value of retention. And he makes a strong case for the importance of this measure to SMB SaaS. I think there is value in tracking both types of churn depending on your SaaS business model. For now, think about the messages that these two measures of churn could be sending:

Make no mistake, churn is an important metric for any SaaS business. David Skok outlines the importance of churn in this classic article. And he continues by describing the growth that results from so called negative churn. But all he is saying is that increasing revenue from existing accounts is a powerful growth lever. Growing revenue from existing customers

Both upsell and account expansion are ugly and jargonistic English so let me drop them now. We are talking about selling more to your existing customers. Either by increasing the number of users a customer pays for. Or by raising the value of the services your SaaS provides to those users. Often the revenue added will be a bit of both.

Measuring this type of revenue communicates an entirely different type of message:

Growing revenue from your existing customer is a powerful growth mechanism. Tom Tunguz argues in favour of negative churn on this basis. But recognises at the end of this intelligent article that this does not give the whole picture Two whites offset to make a black hole

The heart of the problem with negative churn is the combination of these two factors. Offsetting one against the other loses the messages that each is trying to send. Without offering any new value in return.

Sure, if churn turns negative it proves that your growth from existing customer is more than you lose from customers who cancel. So what? At the same time you could be missing:

Contrast this with LTV which also combines two measures. Revenue per customer and customer lifetime. Here both point in the same direction. And are supported by a common goal of better customer satisfaction and loyalty. Sound maths doesn't mean a good answer

Maybe part of the reason this metric has been promoted is that both elements affect LTV. David Skok has demonstrated in LTV - DCF provides the answer how the sums can account for both factors in your LTV calculation. He has even thrown a discount factor.

There is nothing wrong with David’s maths. But LTV is a summary measure. Once you have it, you break it down if you want to find the areas to make improvements. And in that breakdown the factors in negative churn apply in different places. The value part of LTV is based on average revenue per user user/ account (ARPA/ARPU). If you grow the revenue earned from accounts over time, this value will increase. A good thing and well worth managing. Revenue growth from existing customers is an important part of this mix. Lifetime is the inverse of churn (1/ Churn %). If churn is a genuine negative this is mathematically impossible. So even in the Skok formula you need to use the customer churn rate. In other words lifetime needs to be as accurate a reflection as possible of how long a customer stays with your SaaS. Building longer term relationships with customers is also a great thing to manage. And that is where the other half of negative churn comes into play. Focus on building a great business

Negative churn is not an accomplishment. It is not a real metric at all. It reminds me of Boris Johnson’s policy on cake. 100% pro having it and 100% pro eating it. Great fun but not that useful in the real world.

Tangling two things together means you could be missing what really matters. You risk looking in the wrong direction or misallocating your resources. Your business becomes more fragile. Because you narrow and obscure the voice of your customers. Forget artificial metrics. Focus on growing revenue from your loyal customers. And on extending loyalty by helping customers get the benefits of your SaaS. Listen to separate, clear metrics and learn from everything you hear. Use this to give your teams the right objectives. And put resources where they will add the greatest value. "I can’t tell you why our business is growing

Ali Mese from Growth Supply published this article on Crew a couple of weeks ago. It might be the best post on sales funnels I have ever read. His point is simple. Why worry about the detail of your metrics when you could be creating more value for customers? And he cites plenty of great companies that share this philosophy.

Perhaps though he would not expect confirmation from the boss of Dior. In Lunch with the FT this week Sidney Toledano expressed his view of reliance on numbers: “Some people try to find out what’s wrong through the numbers. But if you stay in the office, nothing will change.” and “…its better to have no explanation for success than a lot of explanations for failure."

This stands in nice contrast to the deluge of metrics matter material hitting startups. Some readers may know that I am not a big fan of this approach. But instead of digging further into why I think its wrong, let me ask a different question.

Why on earth do startups want to measure and manage everything they possibly can? For a start, I seem to remember that being an entrepreneur is about freedom. Fire your boss. Get out while you can. Do more of what you love. And so on. Where is the fun in becoming a slave to numbers and data instead of wages? And if you think that’s fine for founders but you need a system to control the rest of your business? Well I suggest you go back and reread Animal Farm. So next time you feel the need to grab hold of another set of metrics. And manage the hell out of some abstract concept. Think about these three things. Incentives

Both management and leadership are about human behaviour. The task is to get people to do what you would like them to do. Or to inspire them to fulfil their potential. This applies to customers, investors and teams.

The best way to influence human behaviour is through incentives of all kinds. Measurement creates incentives. So metrics can be an effective agent of change. But they are not the only way. And they can have unintended consequences. There is a famous example from India in the days of the Raj. Colonial officials were worried about the growing number of poisonous snakes, mainly cobras. They offered a reward for each dead cobra brought to officials. Locals soon started breeding snakes and then killing them for the reward. Before long there were more snakes than ever. Your challenge is to change things. That is the point of a startup. So the right place to start is how you create a system of incentives that encourage the change you would like to see. Choose each with care and learn from the effects that result. Place any metrics you choose to use squarely in this context. Try to keep the reptile count down. Learning

Startups make an impact when they understand real world problems and build solutions that make a difference. This does not happen in a bijou loft converted into a cool co-working space. You need to leave the startup bubble and go listen to customers.

After change, the next order task is to learn. Data can be an excellent way of learning about customers and markets. But just because you have data doesn’t mean you should use it. One of the greatest errors in management is relying on numbers just because they are there. What about the things you can’t measure? Sometimes the stuff which can’t be reduced to numbers is the only stuff that matters. Don’t use your metrics as a crutch and miss the big picture. It is rubbish to say that you can’t manage what you can’t measure. Good leaders do it all the time. They sense problems in the team. They interpret customer feedback. They listen to advice and weigh the options. Don’t allow metrics to be a substitute for management or leadership skill. Time

Metrics eat time. There is the delay between measuring and reporting. Shorter than it used to be but longer than you think. Then there is the time taken to analyse. discuss and decide. Often productive but the more you do it the fuller your diary looks.

And there is a philosophical paradox. No matter how much someone tells you that their pet metric will predict the future, it is still based on the past. The growth. The change you would like to happen. The success of your business. All this lies in the future. The past speaks in a foreign tongue. How good are you at translating into the language of today? Startups need speed. Almost the only advantage you have over incumbents is agility. The ability to respond faster and better to emerging market needs. Numbers can help. Or clog up your business thoughts and actions. Use the good stuff and don’t let too much data get in the way. Balance

There is a place for numbers. Metrics can provide a valuable indicator of performance. And an early warning flag for problems. But the goal of business is to create wealth. Not to generate good numbers. Focus on the things that matter.

Use your numbers to help you. Aim for a balance. Good management and great leadership requires thinking and action that is both analogue and digital.

I spend a lot of time with startups. Mainly in Scotland. Where we our unique history binds a country on the fringe of the world deep into global innovation. We are proud of our two unicorns. And there are some amazing founders and businesses. Its tough to generalise - I met Alba Orbital who make satellites this week for example. But the most common business model is a subscription SaaS company aimed at SMB customers. That’s why I write about this stuff so often.

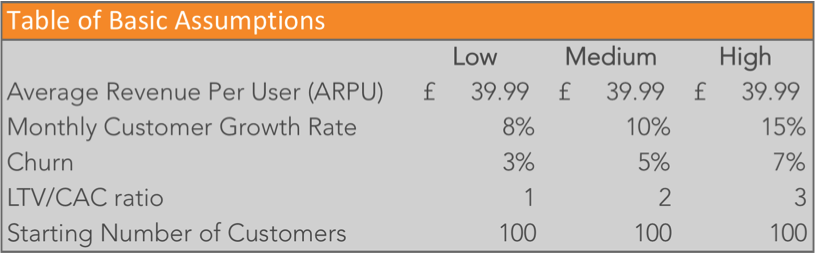

And it niggles a bit that a lot of SaaS analysts focus on the challenges of the SMB market. Every other week I read an article somewhere that argues that you must target the enterprise to achieve SaaS growth. Most of these posts are written by people smarter than me. Yet I can’t get away from a sense that they are missing something. That the economics of SaaS for SMB work. In a niche for sure. But also at scale. I have one fundamental and rational reason for this. SMBs are a huge market. As this Edinburgh Group report shows they contribute 51% of the economy in the developed world and 67% of employment globally . This week I found time to do some digging into the real economics of the businesses that might serve that market opportunity. Here is my thinking on how the unit economics of SMB SaaS could support a great company. Maybe even a few more of those one horned white horses. What do the base numbers for SMB SaaS look like?

As a starting point we need to pick some numbers to model the unit economics. These are averages or benchmarks. Not because you should aim for them. Just to give a representative idea of how a “typical” SaaS business works. The base levels for the analysis below came from:

I have summarised these assumptions in the table below. Showing the high, medium and low (HML) points for each assumption.

What follows is a whole lot of messing around with these numbers. If you don’t have the time or the appetite to follow this take away just these messages:

Analysis 1: Growth rates

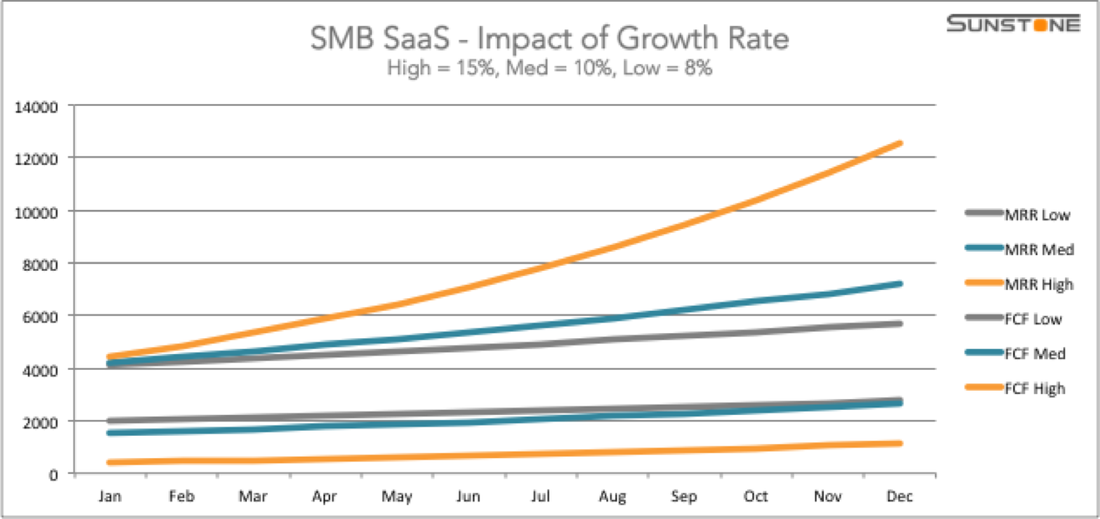

Now let’s start looking at the impact of different trends in some of these basics of unit economics. I will start with the simplest variable which is growth rates. The graph below shows the impact of H (15%), M(10%) and L(8%) growth on monthly recurring revenue (MRR) and free cash flow (FCF). I have used revenue not gross margin. For small SaaS companies storage and processing costs are in effect fixed cost. Not variable with revenue. As you grow you should switch to gross margin for this type of analysis.

FCF is defined as the difference between the cash paid by customers and the CAC spent each month to acquire new customers. In this simple example cash paid and MRR are identical. Because I have assumed all customers pay monthly. We will examine the impact of upfront annual subscriptions later. The other main assumptions are constant across all the HML variables. Churn is 5% in each case, LTV/ CAC ratio is 3. ARPU at £39.99 and opening customer base of 100 are the same for all graphs.

This tells us two things. No surprise that the higher your growth rate, the faster MRR increases. By the end of just one year you can see that the High growth option is pulling away from the others fast. If you play with the numbers you find that 15% is around the minimum for the start of a hockey stick to occur within a year.

FCF works the other way around. Faster growth needs more cash to keep the users flowing in. This would change if the LTV:CAC ratio was better for higher growth instead of fixed at 3. This is an important lesson. High growth can arise either from a more efficient sales model or spending more money. If you are struggling to match the cash raised by your competition, the only answer is to be smarter. And the LTV:CAC ratio is the key metric to track. Analysis 2: Churn

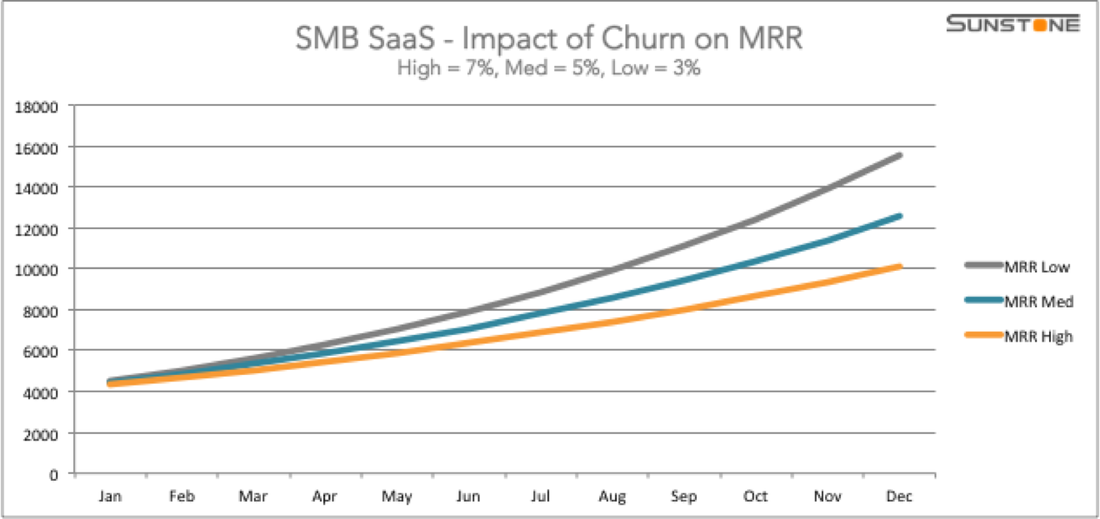

What about churn? Lots of analysts think this is a key factor in SaaS success. Lets fix the growth rate at 15% just so we get a little hockey stick at the end. The graph below shows MRR at H (7%), M (5%) and L (3%) churn.

Here we see a spread of outcome which pretty much follows the spread of churn. Losing customers matters pretty much in proportion to the rate of loss. Keep an eye on churn but don’t get it out of proportion.

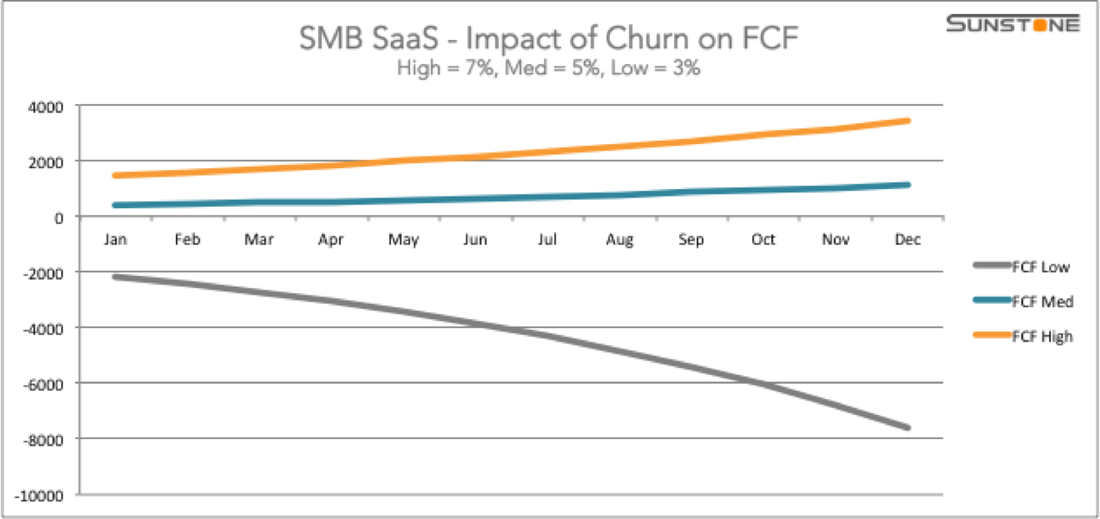

One important caveat. I have used churn in customer numbers here. In a SaaS company where the range of ARPU is quite narrow this makes no difference. But if your highest paying customers represent a significant portion of your revenue then MRR churn matters more. The bigger your customers the higher the likelihood that this will be the case. This will also have a big impact on your sales model. Upsell to existing customers is much more important with an enterprise customer base. Before we leave churn let’s take a look at another effect. If we use the same HML for churn and the same 15% growth rate and fix the LTV:CAC ratio at 3, look what happens to FCF.

Wow! That looks totally wrong. Cash flow gets worse the better churn gets? This is where a small understanding of the dynamics of metrics and ratios could save you a lot of money. Churn is used to calculate LTV. The normal formula is just ARPU/ Churn % = LTV. As a result lower churn gives higher LTV. If we fix the LTV:CAC ratio then higher LTV is an automatic translation into higher CAC .

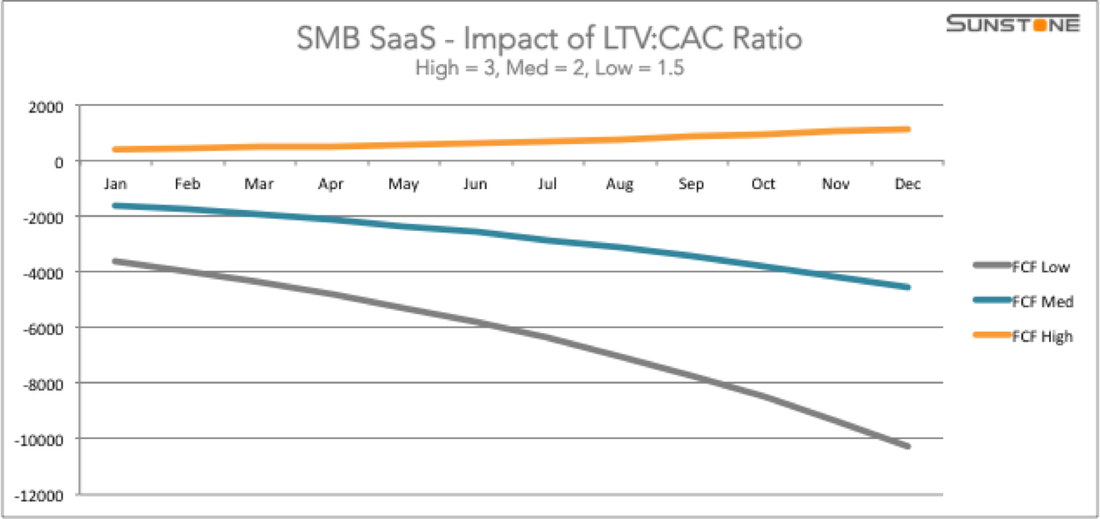

Simple lesson. LTV:CAC ratio matters but so does the absolute value of CAC. If I fixed the value of CAC instead of the ratio we would see the same pattern for FCF as for MRR. Reducing churn is a good thing. But don’t allow your CAC to drift up at the some time by focusing only on the ratio. Analysis 3: LTV:CAC Ratio

Let’s take a look at that ratio. The 3:1 target is rough and ready. Anyone I have read recommends it and then add that there is no rationale behind the number. What impact does it have if we start changing the ratio?

This only affects FCF. MRR does not vary with the LTV:CAC ratio. I have stuck with the 15% growth rate for all 3 scenarios because this is cash hungry. Churn is fixed at the median of 5%. I also see no point in modelling a ratio of 1:1. In this case by definition you are never making any money so something has to change.

It turns out that 3:1 is right on the button. Below this level (1.5:1 or 2:1) cash burns fast. At 3:1 you can stay FCF positive - just. For your SMB SaaS ever to get to cash positive, 3:1 is the minimum ratio. Get there and keep improving is critical to a sustainable business. Analysis 4: Beware the discount factor

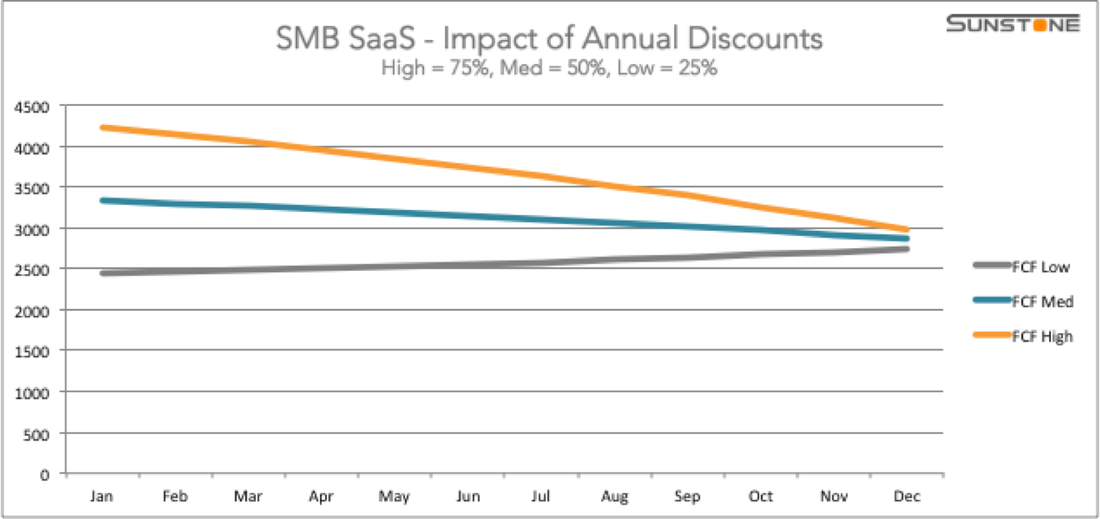

One final analysis of dynamics. Everything so far has been based on monthly subscribers paying every month. Most online SaaS offers packages to tempt payment in advance. Usual approach is a discount for paying a whole year upfront. The argument is that this boosts cash flow. How does this work out in practice?

Another sobering picture. I have fixed the other elements as usual but based on 10% growth. The pattern for 15% growth is the same but extends out over 2-3 years - this allows us to see the effect in 12 months.

The discount element is also fixed. I have assumed 10 months for the price of 12. Again a common approach. The most frequent in the sample of companies I looked at. HML here is about the percentage of new customers paying annual upfront - H (75%), M(50%) and L(25%). The higher percentage gives a big boost upfront. But it narrows fast. MRR shrinks the more you discount. If I laid MRR onto this it would show that MRR in the High scenario was 8% lower than in the Low option. Discounts are for the short term. They can produce a much needed cash boost. But keep your eyes open. The benefit is short and the bar for revenue gets higher with every giveaway. How big does SMB SaaS need to be?

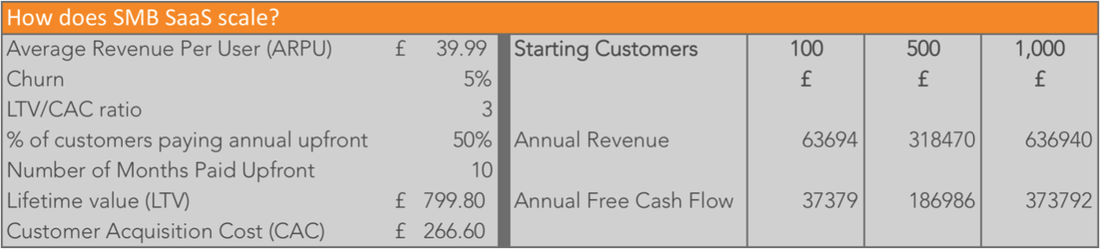

The conclusion so far is simple. The unit economics of SaaS for SMB work. You can generate revenue and cash flow provided your CAC is under control. Yet these numbers deal only with free cash flow. You need to build and maintain a product. Proceed customer service and support. Do all the boring admin stuff that you need to run a business. And make a living for the founders. If each customer is small maybe you need a huge number to make a decent business?

The table below shows monthly and annual figures for 100, 500 and 1,000 customers. Using the mid point numbers for all the other operational metrics.

None of these are unicorn numbers. On the other hand in the context of SMB SaaS they are achievable. Even here in Scotland official statistics show that there are 359 thousand SMBs. Scaling further is great. This show that even 500 customers generates enough cash to make a real living.

To make this work you would need to find the funding to get you to 500. And manage your monthly cash burn within these margins. But it is possible. Working in the real world

These analyses are based on averages. There is no such thing as an average business. Every SaaS will be different. Even the “choice” between SMB and Enterprise is not real. Potential customers occupy a continuum. These rough and ready calculations can help guide you. And provide a bit of fun. They are no substitute for paying attention to the real details of your company.

I have put the assumptions and calculations I used to generate these numbers into a free Google sheet. You can access this and play with the numbers for your business if you like. Remember this is a simple sheet so you can produce strange effects like the one in Analysis 2 above. And even if your numbers look good you still need to make stuff happen. In the end metrics are just the voice of your business. What they say will depend on the specifics - customers, product, business model. What you do will depend on you listening and acting on what you hear. These figures are only indicators of the possible. Having worked through them I am convinced of three things:

For anyone involved in building SMB SaaS, don’t be distracted or discouraged. The business model works. Its success depends on delighting your customers so stop reading and get on with it. How well do you understand your data? If you run a SaaS business you better have a good answer to this question. Its a truism but SaaS is all about data. Every step of the process is measured and tracked. Pipeline metrics. Growth metrics. MRR v ARR. LTV/CAC ratios. And all the rest. It is a are week when no-one posts a new measurement idea critical to SaaS success.

Many blogs and analyses are published by those who believe this enables a goal setting culture. Set the right targets for key metrics. Build sales and customer success teams that are accountable for those objectives. Establish clear quotas and incentives. Drive the business culture by focus on the right results and you will succeed. This approach is favoured by a lot of entrepreneurs and investors with more experience in the startup world than me. Yet I think there is a different, better way. For me metrics are the voice of your business. Most important that also makes your numbers the voice of your customers. I prefer to listen to the data. Learn from what it tells me. And improve your SaaS using that knowledge. The only trouble with this philosophy is that many people don’t know how to listen to their data. Even those with great numeracy and technical skills. Using and understanding metrics is a different skill from doing the calculations. You can read a fascinating and moving article about the common mistakes at “Beginner’s Guide To Data Based Thinking”. So when you are faced with a mass of SaaS data, what can you do to understand what those metrics are trying to tell you?

Metrics are a gift for any business. We are lucky in the SaaS world that so many data points are available. The numbers are a guide to many unknowns. They can provide a picture of customer behaviour. Buying intentions. Churn signals. Growth trends. They can show the strength and weakness of every business. Learn how to use your metrics. Listen to them. Ask the right questions. Make better decisions based on the answers. Build a constant cycle of learning and improvement. Benchmarks are a popular approach to business improvement. They provide an insight into how peers and competitors are performing. And identify areas for potential improvement. But they are an average. They highlight the status quo and undervalue innovation. The metric driven nature of SaaS makes it a great model for benchmarking. Think of this data as useful insight. You can learn from how others perform but don’t copy it. This is another in my series exploring how ideas used by large enterprises might be of value to startups. In this post I am going to explore Benchmarking. Benchmarking or comparison shopping is a popular technique. Many enterprises us it for business performance improvement. It is a big business in its own right. With a subscription model just like SaaS. Gartner and Hackett are built on benchmarking as a service. Every large consulting firm has offered the service at one time or another. The basic principle is simple:

Key TakeawaysThe potential to add value for a startup seems clear. Often founders have little or no data about the market they are entering or their competition. Limited networks and experience create open minds. But they are no substitute for experience of the sector or the business. Used well benchmarking can offer:

The Not So Useful StuffThis all sounds great. But in my experience benchmarking is no more than a way in. It provides an interesting snapshot but not a yardstick or a basis for measurement. I used to have a global client that spent millions every year on industry specific commissioned benchmarks. They cancelled after a few years because they could discern no performance improvement. There are several reasons for this. It is worth thinking about the following whenever you look at a benchmark or similar report.

Next StepsThere is an emerging industry in SaaS around benchmarks. The metric driven nature of the business model lends itself to this approach. I would suggest a startup pays little attention to this stuff. It is nice to see something and think you are doing better than the competition. But after the warm glow its adds no value.

The best way to view this is like an insider blog post. Useful background and a point of view but not the absolute truth. Learn from benchmarks but don’t copy them. If you are entering a market with established competitors it may be a handy way to learn about the competition. But don’t pay for it. Money is scarce and this will not be a good use. Focus on finding the metrics that drive growth and development in your startup. Work to improve on those measures and the competition will not be a problem. For more of the best business thinking for SaaS, subscribe to our newsletter.

A startup I know well posed an interesting question this week. The company is raising seed funding. The founder has taken a cautious path so they have good traction and a revenue model. Nonetheless this is their first formal round. One of the potential investors is unsure of the valuation. Said investor is proposing a discounted cash flow (DCF) valuation.

DCF is a well known and respected technique. Analysts use it to value companies and long term projects every day. What is it? Wikipedia has this definition: In finance, discounted cash flow (DCF) analysis is a method of valuing a project, company, or asset using the concepts of the time value of money. All future cash flows are estimated and discounted by using cost of capital to give their present values (PVs). The sum of all future cash flows, both incoming and outgoing, is the net present value (NPV), which is taken as the value or price of the cash flows in question.

This is crazy

The investor who thinks this works for any startup is crazy. The basis of DCF is a forecast of future cash flows. Startups operate in a world of complete uncertainty. Forecasting revenues is near impossible. When I review startup business plans, I am interested in the financial forecast. But I am looking for messages about ambition, traction and product/ market fit. I don’t place any reliance on the actual numbers.

If you look closer you will see the little word “All”. Proper DCF uses all future cash flows. Most startup business plans only include 3 year forecasts. I have seen DCF valuations of capital projects that cover 20, 30 or even 50 years. At seed stage most startups do not even survive the 3 year horizon.

Kissing Cousins

Small Business Consulting Gets Technical

If you get this, it is easy to dismiss DCF. Irrelevant in the startup world. I agree that it makes no sense as a basis of valuation. But I think it does hold some lessons for a SaaS business. The reason? Consider the parallels with lifetime value (LTV).

LTV is one of the core SaaS measures. In concept it is just like DCF. You calculate the revenue or gross profit for each customer. Over the life of that customer. Your LTV is the sum of the future expected revenues from each customer. Then calculate an average to give an individual customer LTV. This is a newer and less developed way of measuring value compared to DCF. What lessons can we learn from LTV’s older, more grown up cousin?

“Discounted by using the cost of capital” covers several things. Including some reasons not to use DCF for a startup valuation. The words are bit of financial jargon. So the best way to illustrate this is by unbundling the terms.

Lifetime

On the surface LTV is better than DCF at estimating lifetime. In many calculations there is no fixed lifetime for DCF. Churn puts a time horizon into every LTV number. The maths of using churn this way makes sense. But it hides an important truth. Churn happens to the customers that leave. In every cohort there are customers that stay around. These accounts are gold mines.

Mobile network operators discovered this early. Your average customer is an expensive habit for an MNO. He or She changes the handset every 2 years. This means an extra customer acquisition cost. Often linked to a drop in monthly revenue. Some people don’t do this. They keep that old Nokia forever. Many love those things. The monthly line rental and the call package just keep rolling in. You can make an simple calculation of the impact of this. Take a typical SaaS SME customer paying £50 subscription every month. The company has nice ow churn of 1% per month. The average LTV formula is: LTV = MRR X 1/CR where MRR is monthly recurring revenue and CR is the churn rate. For our example customer this gives LTV of £2,500. The technical term for revenue which keeps going forever is perpetuity (P). The formula for calculating the value of a stream of payments in perpetuity is: P = MRR/IR where IR is the monthly interest rate or cost of capital if you have that number. Imagine an interest rate of 10% per annum. High by today’s standards. Above the range of 4-8% quoted in this article from Forbes last year. Using this rate P is £6,000. The customer you keep is worth almost 2 and a half times the average. Before you factor in the extra customer acquisition costs involved. Remember you have to replace every user who cancels a subscription.

Cost of Capital

Applying calculated values for cost of capital makes no sense in the startup world. The uncertainty overwhelms the logic. Thinking about how to approach this provides a great frame of reference for some big decisions.

Time value of money is real. A dollar today is worth more than a dollar in a year’s time. But the difference is not infinite. Discounts to encourage people to pay for a year or more upfront make sense. The cash upfront can be a lifeline for a startup. Dry interest rates don’t capture the value that represents. You do need to think about what works when pricing up your product. Capital structure is not a relevant factor. The startup parallel is opportunity cost. Or cost of choice if you prefer. Again not something to wrap up in a percentage rate. But think about adding features, tackling new markets and so on. Early doors the question is which option brings the best return. As you become established this changes. Now you need to ask a different question. Will investing in something new earn a good return? Is it better to put more resources into your proven business model? Weighing up risk is one for the future. Every step on the startup journey is high risk. A founder cannot be reckless but risk analysis can lead to paralysis. Be aware but don’t lose the bias to action.

Building a scalable SaaS recurring revenue model is neither art nor science. Skill and judgement play a part in every decision. A rigid set of rules and boundaries has little meaning. A framework that helps your team recognise the context of your choice can be a big help.

Professional finance managers have developed some great techniques. DCF has an important place in this arsenal. The basis of these models is valid theory and sound maths. The variables involved kill the benefit for a startup. Understanding how established methods work can still provide valuable lessons. The core SaaS concept of LTV is a cousin of DCF. Looking at both is illuminating. No two SaaS businesses will be the same. Within any business, the context of each decision will also be different. No advisor can lift the load of making tough decisions from an entrepreneur. Great small business consulting for a startup means helping founders make those choices better. Helping new leaders learn their craft. Subscribe for more insights direct to your inbox. Learn the Startup Craft to Build Your Revenue Model

LTV or Customer Lifetime Value or CLV is one of the key SaaS Metrics. It is a simple and powerful measure which is essential to the startup financial model. There are slight variations in definition but only a few essential elements. A quick primer/ reminder:

Keep it Simple - Use the Definition that works

Search for LTV and you will find a surprising number of articles with titles like “Why is your LTV wrong?” or “Mistakes everyone else makes in working out LTV.” There are a lot of nuances to LTV. My view is simple. Use the formula which makes most sense for your businss. Getting value out of the metric is about listening. Not about picking holes in the detail.

Learn to Listen if You Want Answers

What can LTV tell you and how can you use that information? For many businesses the measure is a way of evaluating marketing strategies. Others use it to forecast revenues and profitability. It also provides a window on the customer lifecycle.

All valuable insights. All available if you learn how to listen. Startup consulting and startup tools offer ways to answer these questions. Trouble is lots of people think the metric is telling you. To get the benefit you need to be more subtle. Think of it like listening to feedback from your boss. The body language, context, timing and language are essential to understanding the message. SaaS Metrics for SMEs - What is LTV saying?

3 Smart Ways to Use LTV

Some SME SaaS specifics to watch for when listening to LTV:

LTV is a great source of insight into your business. It is not a single source of truth. Every customer is an individual.

Be smart about LTV by doing three things: Listen to the signals and make strategy decisions based on what you hear. Treat every customer as an individual and make sure your interactions stay personal. When you lose a customer or fail to convert a free trial, be nice. There is every chance that customer could be back. If you want to know more about using LTV as a tool for listening to your customers and making better decisions, subscribe below. Good luck. What the experts sayI read a great post from AdEspresso recently. Its about churn in SaaS startups that are selling to SMEs. In simple terms, high churn in the first 3 months of use is just part of the sales funnel. 5% churn or higher will not kill the business. Once through this early period, users will stick around. I work with a lot of SaaS companies and most of them target the SME market. This got me thinking about the economics of these businesses. I started to look again at the best SaaS sources. Tom Tunguz, Jason Lemkin, David Skok and others have written a great body of work on SaaS metrics. But it is all about selling to the enterprise. They talk about CLV or annual revenues in the 10’s even 100’s of thousands of dollars. The main element of customer acquisition strategy is people. Marketing, sales and customer success teams. Look at this post on the fundamental unit of growth for example. This is not the same world that many startups live in. This took me back to what has helped SaaS companies succeed in the SME world. The first thing I noticed is that the basic framework of SaaS metrics remains the same. Customer Acquisition Cost (CAC), Growth, Monthly Recurring Revenue (MRR), Customer Lifetime Value (CLV) and Churn. It is only when you dig into these numbers that the differences emerge. Customer Acquisition Strategy is the first differenceStart with CAC. Accepted wisdom is that sales efficiency (CLV/CAC) runs around 0.8. Anything over 1.0 is considered good and 2.0 is best in class. Coupled with high churn, this level of cost makes selling to SMEs look very unattractive. But this is not the reality. SME SaaS can achieve sales efficiency ratios of 5 or even 10. It just costs less to get a new revenue dollar.  There is a simple reason for this difference. Enterprise SaaS requires sales teams. Tom Tunguz post above lists Sales Development Reps, Account Executives, Customer Success Managers and Upsell Reps. SMEs need none of this apparatus. In fact they hate it. Small business owners are far too busy to spend time talking to reps. Once they have a a product they just want it to work. They don’t expect or want regular account calls. The recurring revenue model does not depend on direct sales. This doesn’t mean marketing, sales and support don’t matter. It does mean that the product and onboarding process needs to be friction free. Most of your customer acquisition will be online. So you need to learn what works. How you reach the right online audience and how you convert with minimal intervention. Partnerships or integration with parallel products can also be part of the mix. Keeping CAC low and Sales Efficiency high is an art form. CLV is linked to the recurring revenue modelCLV is another major difference. For an SME this number will be much lower than for an enterprise. The revenue models are different. At its most basic this means you need more customers to make a viable business. With SMEs there will also be much less opportunity for upsell. Service revenues from installation will tend to be nil. Growing CLV means you need to keep customers loyal. You need to embed your SaaS product in the life of their business. Be too good for anyone to risk a change. ...and finally churnThat brings us back to the final element as pointed out by AdEspresso. Churn rates can look high. The idea is that this is part of the sales funnel. It should be combined with conversion rates. The success of early months for an SME customer also depends on the onboarding process. Remember this is unlikely to generate much if any revenue. Yet managing your customers through this process is critical. Building a frictionless product is half the battle. Investing in people to help your customers will also pay dividends. Far more than a sales force. Onboarding is the secret of successWhat is the secret of a a great on boarding process? Des Traynor from Intercom wrote recently about the evolution of onboarding. In today’s world there is one key - change. You want the small business owner to adopt your product. He or she needs to change something. It can be a change in business process. A change in time allocation. Even a change in lifestyle. Your on boarding process needs to help your customer change. It also need to link that change to success for their business. To find out more about SaaS metrics and to receive a free copy of my SaaS Revenue model tool, subscribe below.

|

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016