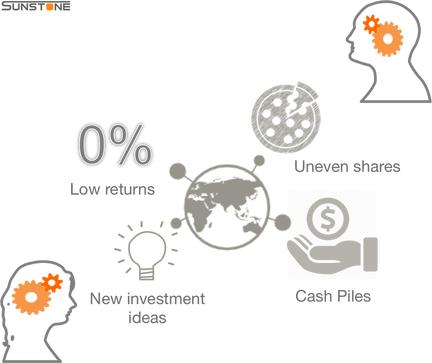

This is part two of a series of three articles on the impact of a bust in startup valuations. For part one read down below. For part three…be patient. Valuations and the real economyMattermark published a fascinating blog post in January. It explores the connection start up investment and US interest rates. Do historic low rates fuel explosive growth in funding? The article explores various trend correlations which support some basic economics. Extreme low yields (zero in the case of interest rates) will give a high nominal price. For any stream of earnings. Fred Wilson of Union Square Ventures explained the theory in depth in March 2014. 0% Interest drives high startup valuationsThis essential fact lies behind one of 3 megatrends. Together these have created the current funding landscape. Another way of looking at the first trend is to consider alternative forms of investment. Look at four major traditional options. Public equity markets, public debt markets, property and physical assets, and business investment. Returns on the first two categories are at historic lows. Debt markets are flooded by Government debt. Real interest rates have turned negative in many countries. Stock Market Indices are high but this reflects a lot of money chasing a small pool of return. P/E ratios are also in record high territory. The picture for property appears more mixed. This is because the focus tends to be on capital values. But the explanation for the rapid recovery of property values is the same. It is a reflection of diminishing returns. I admit that this trend is patchy with a heavy concentration in narrow markets. Think London and Silicon Valley. Cash is piling upBusiness investment is a window on two of our megatrends. In most developed economies, levels of business investment remain low. Business owners are refusing to invest because the returns are too low. Many corporations have huge piles of cash on their balance sheets. But they are not spending. The supply of cash is growing at an amazing rate. The US, UK and Japan have all printed epic amounts of money in the last 5 years. The US is now calling a halt (or at least a pause) but the EU is just about to start.  This cash is not distributed in a broad or deep spectrum. The mechanism of QE is not a direct one. As a result, most of the printed money is sitting in 3 places. Corporate balance sheets. Sovereign wealth funds from commodity producing countries. And non banking financial institutions. Policy and regulation are keeping banks starved of funds. At the same time both private and public investment vehicles are awash. Little or nothing is trickling down to the bottom of the pyramid. Thomas Piketty’s treatise on inequality is a thorough reflection of this trend. New investment opportunities emergeA huge increase in cash concentrated in few hands. Historic low returns on many forms of investment. These trends create the conditions for massive investment in new structures and forms. This is exactly what we see. Our third megatrend is the current startup funding world itself. It is different from previous booms. Money is being invested through private vehicles. Much of the cash is institutional, corporate or from wealthy individuals. But it is hidden from the public markets. This means there is no liquidity. Investors cannot retrieve their cash. As Mark Cuban points out in this post, a fall in valuations of investments with no liquidity will be very painful. Where will the signal come from...This was going to be two articles about the impact of a correction in startup valuations. "Why the startup funding bust will be a beautiful thing” looked at the impact of a bust on startups. Part three will look at the wider economic and social changes a bust might bring. When I started writing I discovered that I needed this bit as well. Context is important. Changes in the direction of these trends will be the signal for the correction. When this signal is sent and how long it takes to transmit are big unknowns. In one view it could take a long time. In Europe the situation looks just like Japan 30 years ago. That has not unravelled yet. This applies to all Europe not just the Eurozone. The UK happens to be ahead but... We live in a dangerous worldOn a different view a dramatic turn could happen fast. The current fall in the oil price might be that early signal. Severe disruption caused by political factors is also a live possibility. Public statements from politicians and the media are depressing. In proper democracies are led by people who appear to understand nothing. Public discourse about the challenges on the borders of Russia or in the Middle East is verging on puerile. To describe most media coverage as First Grade level would be an exaggerated compliment. Other possible flashpoints - West Africa, the Horn of Africa, Korea/Japan, SE Asia. Not even on the radar. Startups could cause their own downfallWe must also acknowledge that startup ecosystem could be the cause of its own bust. People have come to rely on software in both personal and business lives. Many apps are interconnected in a web of APIs and integrations. A severe failure in the wrong place could cause massive disruption. Loss of trust and faith would cause investors to hold back. Valuations would fall.

Failure is not the only possible problem. There is a whole industry of naysayers just waiting to jump on a privacy breach. Security and integrity are vital to all our futures. Even a small problem could be magnified in the wrong circumstances. Again the issue is loss of trust and faith. Investment depends on sentiment as well as spreadsheets. Watch with interest. Tech start ups live in a global economy. It is one of the benefits of the digital revolution. That brings responsibility. Everyone in the ecosystem needs to pay attention to global trends. I am not an economist or an “expert”. My view could be way off. But there will be a down turn. I would love to hear what innovators and entrepreneurs think could be the cause.

Comments

|

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016