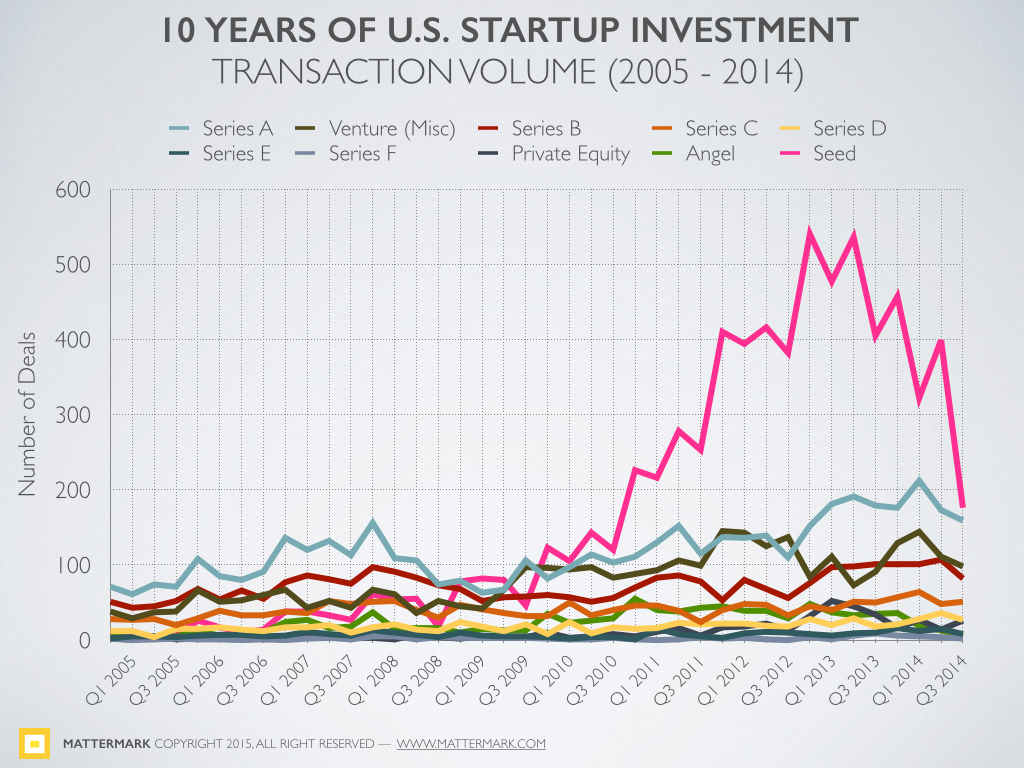

On the surface the investment outlook for technology start ups has never been better. VCs invested $48.3Bn (Money Tree Report) in US start ups last year, a whopping 60% increase year on year. Most of this torrent of cash went into software and biotech companies. Start up investment has become one of the hottest business trends across the world with Governments and commercial bodies vying to establish incubators, accelerators and other schemes. Seed funding is actually fallingA couple of recent reports have highlighted a trend underlying this growth which gives cause for concern. Mattermark (@mattermark) published an analysis of all funding rounds in the US over the past 10 years which shows the number of seed rounds falling from a peak in Q1 of 2013 back to 2010 levels. CrunchBase (@crunchbase) has taken this further and looked at data from the next 7 largest countries by number of Internet users. Both the number and value of seed rounds have dropped significantly in 2014. Investment is shifting from seed rounds to large Series A or later financing. What is happening?I don’t believe there is any shortage of innovative ideas and new entrepreneurs entering the market. If anything I expect that statistics on new business starts will show tremendous growth once again in 2014. Many of these start ups will share the ambition and commitment of their recent predecessors. This is one of the roots of the trend towards larger, later financing. Building a world leading company takes time and money so investors are in a longer cycle. Investing larger amounts for longer cycles also puts a strain on investment capacity. Start ups have attracted funds in recent years because other investment classes have offered very poor returns. As traditional investment options start to recover in at least some large countries, especially the US and UK, this inflow of new funds may slow. Anecdotally, I know of a number of Angel syndicates and VCs who are mainly preoccupied by follow on rounds. Follow on investment may also be going to quite well established businesses with a proven and profitable business model. Such companies just need working capital to fuel growth. This role has traditionally been filled by bank lending but at least in the UK there is little sign of this tap being turned back on. As a result, more funding from private sources is occupied with companies at this stage of maturity. It would be very interesting to see data on the level of exits. Larger investments with longer payback cycles will ultimately lead to a shortage of liquidity which will put further strain on the front end of the investment chain. Why is this a problem?The risk is that a funding gap emerges. Founders will continue to bootstrap and incubators will provide enough resources to allow all sorts of people to get companies started. VCs and other private investors will continue to show interest in companies that have a viable product and some traction. Bridging the gap between early stage accelerators and product launch/ validation could become a real problem.

Tech EU is currently running an excellent series on companies that have grown large without any recourse to external funding. You can see the latest instalment about Cleverbridge here. Are we entering a phase where managing without investment will become a key business skill? I would love to know. Are you seeing the same trends in start up investment that these reports highlight?

Comments

|

Categories

All

AuthorKenny Fraser is the Director of Sunstone Communication and a personal investor in startups.

Archives

September 2020

|

RSS Feed

RSS Feed

Learn more |

Contact |

©Sunstone Communication Ltd 2016